As we approach year-end, it is your last chance to implement strategies that can help reduce your tax bill for this year. With the passage of the One Big Beautiful Bill Act (“OBBBA”) this summer, there are a few key provisions to keep in mind that can help you optimize your income and reduce your tax liability before December 31.

Key Takeaways:

- December 31 is the deadline for most tax-saving strategies.

- Tax-loss harvesting may offset capital gains and reduce taxable income.

- Realizing capital gains in low tax brackets may offer planning flexibility.

- IRA, 401(k), HSA, and SEP contributions are subject to annual limits.

- Roth IRA conversions impact future tax brackets and RMDs.

- Required Minimum Distributions must be taken to avoid IRS penalties.

- Charitable gifts using QCDs or bunching may maximize tax efficiency.

- Annual exclusion gifts and 529 plan contributions are part of the wealth transfer strategy.

- Qualified Opportunity Zone investments may defer capital gains.

Harvest Losses from Your Taxable Accounts

Selling securities for a loss (harvesting losses) may help reduce your tax bill now and in the future. Even if you held the securities for less than a year, losses from the sale of securities can shelter short-term and long-term capital gains realized this year from income tax. Keep in mind that capital losses are netted against all capital gains, including those from the sale of a business and real estate. Any unused losses can reduce up to $3,000 of ordinary income, and you can carry forward any remaining unused losses to help reduce future tax bills. Note that you cannot deduct a loss on a security when a virtually identical one is purchased 30 days before or after the original sale, as this is considered a wash sale. Also, if you had significant losses in 2025 or any other prior year, you may have tax-loss carryforwards that can be applied to your 2026 taxes. Know that your Beacon Pointe advisor is working to realize any available capital losses on your behalf prior to year-end.

Harvesting Gains from Your Taxable Accounts

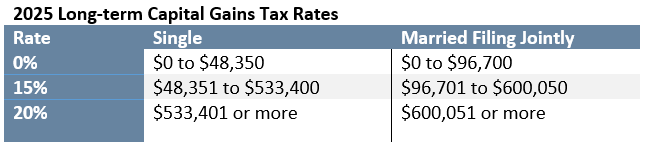

In contrast, if you find yourself in a low tax bracket for 2025, you may wish to take advantage of the lower tax rates on capital gain income. It may benefit you to realize gains from a concentrated stock position to diversify your asset allocation further and increase the cost basis in your overall portfolio. This strategy may also benefit pass-through business owners with an expected net operating loss from their business in 2025.

Maximize IRA and Retirement Plan Contributions

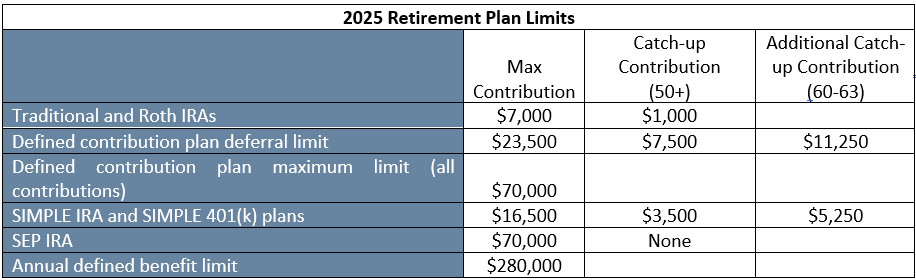

If you are employed, make sure to contribute to your retirement accounts up to the allowed limits. See the chart below for the maximum amount you can contribute to your plan. Starting in 2026, if your income exceeds $145,000, the catch-up contribution will have to be directed into the Roth portion of your retirement account. However, not all employers might offer this option, so it is a good idea to check with your retirement plan administrator. Furthermore, if your employer-sponsored plan allows for post-tax contributions and in-plan Roth conversions, you can defer up to $70,000 in 2025, which includes all company matches and forfeitures. These post-tax contributions create what is known as a “mega-backdoor Roth IRA,” meaning these contributions grow tax-deferred and can eventually be rolled into a Roth IRA, making them potentially tax-free in the long run, subject to IRS rules and eligibility requirements.

If you are a business owner, consider contributing to a SEP IRA or establishing and contributing to a 401(k) plan before the end of the year, as doing so helps you defer and reduce your business taxable income. See the chart below for the maximum amount you can contribute to your plan. For SEP IRAs and profit-sharing/401(k) plans, the contribution limit is 20% or 25% of compensation (depending on the type of business entity), up to a maximum of $70,000 for 2025. Deferring income may allow you to qualify for a 20% qualified business income (QBI) deduction on your business income. This deduction can potentially apply if deferring the business income brings your total income below the applicable income phase-out threshold.

Note that the deadline for making IRA and Roth IRA contributions for the tax year 2025 is April 15, 2026.

Convert Your Traditional IRA to a Roth IRA

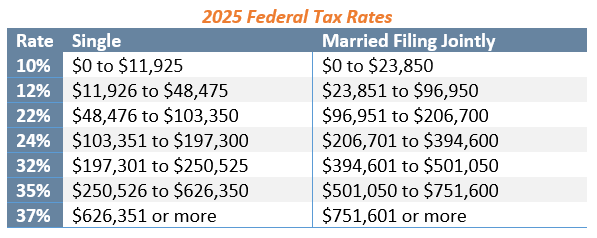

If you qualify for the enhanced seniors deduction of $6,000 under OBBBA or anticipate that your tax rate may be higher in the future due to expected increases in income or higher tax rates, consider converting a portion of your traditional IRA (or other qualified retirement accounts) to a Roth IRA. A Roth IRA is appealing as qualified withdrawals from a Roth IRA are tax-free, unlike distributions from a traditional IRA. Market downturns can also be a great time to convert to a Roth if your IRA has declined in value as converting it means you’ll pay income tax on the lower current value, and enjoy any subsequent tax-free recovery within the Roth IRA. Additionally, reducing the balance of your traditional IRA through conversion can lower future required minimum distributions (“RMDs”), potentially decreasing your taxable income and minimizing the impact on Medicare premiums and Social Security taxation. However, it’s important to remember that conversions are taxable events as you’ll owe income tax on the amount converted. A Roth conversion tends to make sense if (1) you can pay the taxes from funds outside your IRA, (2) expect to be in a higher tax bracket later, (3) plan to let the funds grow for years, or intend to leave the account to your heirs. Keep in mind that once you convert to a Roth IRA, you cannot undo the conversion as you could in the past; also, it may inadvertently cause you to miss out on some deductions or unfavorable tax consequences. It’s advisable to consult with your tax professional before deciding to convert.

Take Minimum Distributions from Retirement Plans

If you haven’t done so already, make sure to take your required minimum distributions (RMDs) from your IRA(s) or qualified retirement plan(s) before December 31, 2025. The IRS mandates that a minimum amount must be distributed from retirement accounts each year. It’s important to note that the RMD age was changed with the passage of the SECURE Act 2.0, moving from age 72 to age 73 and is set to change again in 2033 to age 75. If you fail to distribute the required amount, you will face a penalty of 25% (10% if corrected timely) on the amount that should have been withdrawn but wasn’t. Remember, RMDs are not required for Roth IRAs. If you were born in 1952, you are age 73 in 2025 and will need to take your first RMD. The latest you can delay this first RMD is April 2026, but be aware that you will then need to take two RMDs in 2026. This approach may be beneficial if you anticipate having a higher income in 2025 and expect lower income in 2026. We recommend having income taxes withheld from your IRA distributions to help with cash flow planning.

RMDs may also apply to certain inherited retirement accounts. The primary factors that determine whether an RMD must be taken from an inherited retirement account, as well as the timing and requirements, are as follows: (1) the date the account holder passed away, (2) the beneficiary’s relationship to the deceased account owner, and (3) the type of retirement account inherited. For more information, read our pieces on FAQs About RMDs or So You’ve Inherited An IRA.

Charitable Giving

Because of the OBBBA, starting in 2026, taxpayers who itemize deductions will face a new limitation on charitable giving as only contributions exceeding 0.5% of adjusted gross income (AGI) will be deductible. This new “charitable floor” and the new cap on total itemized deductions will certainly affect those in the 37% tax bracket, making strategic consolidation of deductions more critical than ever. By bunching charitable gifts and other deductible expenses before the end of 2025, you can maximize your deductions and preserve valuable tax benefits. Creating a donor-advised fund can be an effective way to achieve philanthropic goals while also providing financial benefits through tax deductions. Other strategic giving, such as donating appreciated assets or donating your RMD through a qualified charitable distribution (QCD), can further reduce taxable income and ultimately lower the overall tax liability. For more information, read our piece on Thoughtful Charitable Giving to help make your charitable giving the most impactful.

Make Annual Exclusion Gifts to Family

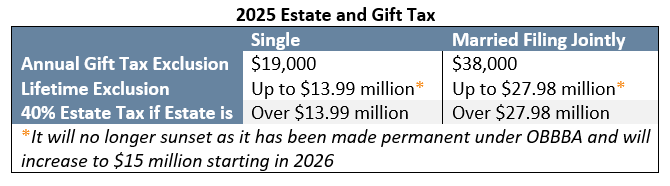

For those who want to help family members, consider making annual tax-free gifts to loved ones. The 2025 annual exclusion allows you to make tax-free transfers of $19,000 per recipient in cash or property without reducing your estate and lifetime gift tax exclusion amount. Married couples can give $38,000 to each child, grandchild, or anyone else using the annual exclusion. These tax-free transfers do not require filing a gift tax return (unless you split gifts with your spouse). Gifting shares of stock or other investments can get them interested in learning about investing and can reduce the temptation to spend it. If gifting cash, be sure checks are deposited before year-end to count for your 2025 annual exclusion.

Consider creative ways to give to your children and grandchildren, such as funding college or a loved one’s retirement. You could use an annual exclusion gift to fund a tax-advantaged Section 529 college savings plan. 529 Plans have a special provision that allows a “super annual exclusion gift,” where you can elect to gift five years’ worth of annual exclusion gifts at once (gift tax return required). This strategy would allow gifts up to $95,000 or $190,000 if married in 2025 into a 529 plan. Under the recent OBBBA legislation, the allowable annual withdrawal limit from 529 plans for qualified K–12 education expenses will increase from $10,000 to $20,000 beginning next year. Additionally, the expansion of qualified K–12 expenses, such as books, tutoring, and online learning materials, took effect in July 2025.

. You can now use these funds to cover a wider range of educational expenses beyond just tuition. This includes costs related to primary and secondary education, such as textbooks, tutoring, and other educational materials, as well as expenses for qualified credential programs. If there are any unused funds in a 529 plan, you may be able to roll them over into a Roth IRA for the beneficiary. Remember that there is a lifetime limit of $35,000 for these rollovers, and the 529 plan must have been open for at least 15 years. Speak with your financial advisor for more details.

Read our piece on Financially Savvy Gift Ideas for other creative gifting ideas.

Maximize contributions to HSA Plans

If you are enrolled in a high-deductible health plan (HDHP) and have a Health Savings Account (HSA), consider maximizing your contributions. The maximum contributions allowed are $4,300 for individuals and $8,550 for families, with an additional $1,000 catch-up contribution for those aged 55 and over. You have until April 15, 2026 to deduct contributions made to your HSA for the 2025 tax year. Additionally, make sure to submit all receipts for your HSA for reimbursement. If you have already met your health insurance deductible for the year, consider completing any additional medical procedures before the year ends.

Consider Investing in a Qualified Opportunity Zone (QOZ)

Investing realized capital gains into a QOZ fund allows the investor to defer tax on capital gains realized within the last six months until December 31, 2026. Additionally, it may provide the opportunity for tax-free growth on any appreciation of the QOZ fund investment as long as you hold your interest for at least ten years. The law allows (1) federal tax deferral of capital gain invested in a QOZ until the earlier of when the fund is sold or December 31, 2026, and (2) federal tax avoidance on investment gain on the initial QOZ investment if held for at least ten years. The capital gain deferred or avoided might still be taxable at the state level, and the federal income taxes will be due with the filing of the 2026 tax return. You must reinvest capital gains within 180 days after the gain was realized, or longer for certain pass-through entities. The investment does not have to occur in the same calendar year to qualify for deferral. Make sure to confirm timing deadlines with your tax advisor. It may be wise to postpone any capital gains until after 2026, as OBBBA introduced a revised framework with a new set of QOZ rules with additional tax deferral for investments made starting in 2027.

2025 Key Federal Itemized and Standard Deductions

The standard deduction has been increased this year under OBBBA and is now $15,750 for single filers and $31,500 for joint filers. If your itemized deductions exceed the standard deduction, you should itemize. Key itemized deductions:

- The SALT limitation (state and local taxes) was increased to up to $40,000 combined for taxes paid (property tax, plus your choice of state income tax or sales tax), but begins to phase down once your income exceeds $500,000 and the limitation reverts to $10,000 when your income surpasses $600,000

- Mortgage interest on primary and secondary home loans up to $750,000; loans taken on or before 12/14/2017 up to $1,000,000*;

- Unreimbursed qualified medical expenses in excess of 7.5% of adjusted gross income; and

- Charitable donations

If you could benefit from a conversation with our advisory team, we would be happy to provide a complimentary consultation.

Important Disclosure: This report is for informational purposes only. Opinions expressed herein are subject to change without notice. Beacon Pointe has exercised all reasonable professional care in preparing this information. The information has been obtained from sources we believe to be reliable; however, Beacon Pointe has not independently verified, or attested to, the accuracy or authenticity of the information. Forward-looking statements are based on current legislation. Future changes may impact the applicability of these provisions. Nothing contained herein should be construed or relied upon as investment, legal, or tax advice. All investments involve risks, including the loss of principal. Investors should consult with their financial professionals before making any investment decisions. Past performance is not a guarantee of future results.