Charitable giving not only improves the lives of others but has been shown to increase happiness more than personal spending on oneself.[1] We have summarized the key factors to help make your charitable giving the most impactful.

Key Takeaways:

- Charitable giving can increase well‑being and connect support to causes that matter.

- Choosing charities that align with individual values and causes is a foundational step.

- Researching organizations through independent vetting sites helps understand how donations are used.

- Visiting or volunteering with charities provides direct insight into their operations.

- Recent tax law changes (One Big Beautiful Bill Act) affect eligibility and limits for charitable deductions beginning in 2026.

- Types of assets that may be donated include cash, appreciated securities, real estate, and life insurance policies.

- Donor‑advised funds allow giving over time with a deduction in the year of contribution.

- Qualified charitable distributions (QCDs) enable IRA‑to‑charity transfers that can count toward RMDs.

- Simple gifts such as time, clothing, or regular small donations are also ways to support charities.

Choosing a Charity

We recommend finding a charity that aligns with your values. Begin by searching for charities that help causes that are important to you. Searching on websites like candid.org, givewell.org, and greatnonprofits.org can provide details about how the charity uses the donations. After finding a few charities that inspire you, we recommend scheduling on-site visits to your top charities and interviewing managers involved with the charity before making any significant gift. If time allows, volunteering is a great way to get to know the charity and to see firsthand how they run their business and whether they accomplish their stated goals. You might ask your children and grandchildren to volunteer with you for a few hours to share the benefits of giving back and create lasting family memories. Community foundations are another good way to connect to local charities, as the staff can provide further details of charities working for causes you may want to support.

Maximize the Tax Benefits from Giving?

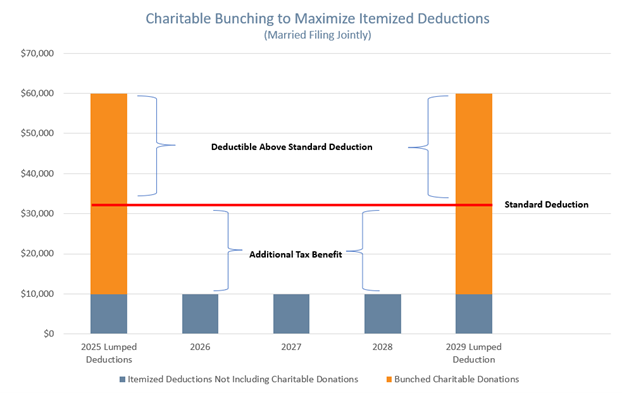

With the passing of the One Big Beautiful Bill Act on July 4, 2025, there are a few changes to deducting charitable donations. Beginning in 2026, taxpayers who take the standard deduction can now deduct up to $1,000 in cash donations (or $2,000 for those filing jointly) to certain charities above the line. This deduction is in addition to the standard deduction amounts for 2025, which are $15,750 for single filers and $31,500 for married couples filing jointly. Larger donations to 501(c)(3) charities result in an itemized deduction, which reduces taxable income for taxpayers who itemize. Also beginning in 2026, there is a new .5% floor, or hurdle, that charitable donations need to exceed to be deductible. This means that beginning next year, there will be a (relatively small) reduction in tax benefit for itemized charitable donations. For some clients, it may be a good idea to accelerate charitable donations before the end of 2025 to maximize the tax benefit. Additionally, the best way to give might be to switch from giving annually to giving every few years. “Bunching” two or three years’ worth of charitable donations into one year might result in itemizing deductions in that year while taking advantage of the now higher standard deduction for the other years (example of married filers in the chart below). Cumulatively, this results in greater tax deductions, which translates to tax savings. If you would like to bunch gifts for tax purposes while benefiting the charity over time, consider using a donor advised fund (discussed below), which allows you to take the charitable deduction in the year of the gift but allows you to make distributions to the charities over time.

Types of Assets to Give

Most gifts to qualified charities, except for the gift of time, qualify for a deduction for taxpayers who itemize. The most common gifts are cash or check, highly appreciated stock, and personal property (including clothes, furniture, books, etc.). But other property such as highly appreciated real estate, cars, old life insurance policies, and qualified direct distributions to charity from retirement plans make attractive giving options as well.

For gifts of cash, inventory, or short-term capital gain property to qualified public charities, the amount of the deduction is the adjusted cost basis of the asset but is limited to 50% of your AGI (60% of your AGI for cash gifts). These limits are based on gifts to qualified public charities, some supporting organizations, and private operating foundations. Gifts to most private foundations are limited to a lower amount of AGI, which may mean a smaller tax deduction. More below.

Long-term capital gain assets like highly appreciated real estate or company stock held for more than one year are great assets to donate because you receive the benefit of a charitable tax deduction, and you also avoid paying tax on the capital gain – the difference between your cost basis and the current market value. Many business owners about to sell their company donate a portion of their company stock to charity before entering into a letter of intent about the potential sale. When structured properly, the business owner may take an income tax deduction [hopefully in the same calendar year when adjusted gross income (AGI) is high] of the fair market value of their company stock donated without having to pay tax on the capital gain. If you give a large donation of long-term capital gain assets to qualified public charities, the amount of the income tax deduction is the fair market value of the asset but is limited to 30% of your AGI. [A special election can be made for long-term capital gain assets that would allow you to deduct up to 50% of AGI, though it limits the deductible amount to the tax basis of the asset donated.] Any contributions above these limits can be carried forward for up to five years.

Large donations to private charities, like private foundations or certain fraternal organizations, are subject to lower limitations. Specifically, the deduction for long-term capital gain property is the fair market value of the assets donated limited to 20% of your AGI rather than 30%. For short-term capital gain property and cash, the deduction is the adjusted cost basis on the assets donated limited to 30% of AGI rather than 50% or 60% for public charities. To determine the deductibility status of the charity you are considering donating to, visit the IRS website https://apps.irs.gov/app/eos/.

If you have a life insurance policy that you no longer need, consider the leverage of donating it to charity. Life insurance policies are great to give because they do not affect your cash flow as an out-of-pocket expense, you get a current income tax deduction if you itemize, and the eventual benefit to the charity is usually much greater than your previously incurred cost. A donation of a life insurance policy to a qualified public charity can yield a current income tax deduction of the adjusted basis in the policy, limited to 50% of AGI. To take advantage of the current income tax deduction, you must irrevocably assign all incidents of ownership to the charity. Donations to pay any future premiums should be made to the charity and are also income tax deductible if you itemize. Donating a life insurance policy to a charity should be carefully coordinated by your CPA, insurance company, and charity to ensure the charity retains an insurable interest in the donor insured and the absolute assignment of all rights in the policy has been made.[1]

Alternate Ways of Giving

The simplest way to give to charity is by giving directly to the charity. However, putting thought into the way you give can create flexibility and possibly increase your tax benefits. To make a charitable donation with a lasting impact, consider using a donor advised fund (DAF). DAFs allow you to get a charitable tax deduction in the year you contribute while allowing you to stretch the gifts to charities over your lifetime. From your DAF, you have the flexibility to set up auto payments to any qualified charity or make a gift once a year. You can also experience the joy of giving to others by allowing them to direct a donation to a charity of their choice from your DAF. DAFs are typically inexpensive to set up, and some even have no minimum initial contribution requirement. The contributions can be invested, so even a little can go a long way. Remember, just like any charitable donation, there can be no quid pro quo (the donor cannot receive anything in return for the gifts), and a DAF cannot distribute to a charity to satisfy a personal pledge.

Another alternative is a qualified charitable distribution (QCD): If you are over age 70½, you can donate up to $108,000 (2025) from an IRA directly to a qualified public charity (not a private foundation, donor advised fund, nor supporting organization) to both satisfy your charitable goals and prevent this part of a required distribution from being included in your taxable income. Making a direct donation from your IRA might lower your income and allow you to qualify for lower Medicare premiums and other income tax breaks. Note that contributing to an IRA after age 70½ reduces the amount transferable to a charity as a QCD. A QCD also counts toward your required minimum distribution for the year.

Individuals may now make a one-time distribution of up to $54,000 (2025) from an IRA to a charitable gift annuity or charitable remainder trust. The $54,000 is part of the $108,000 overall limit referenced above. These charitable strategies provide an income stream for the individual during their life, and any excess assets at their death benefits charities.

Charitable trusts are another way of giving but are more complex and expensive to set up and maintain. Charitable remainder trusts provide an income stream to the donors for a set term of years or throughout their lifetimes and ultimately leave the remaining assets to a charity. A charitable lead trust pays income to a charity during the donor’s lifetime, and the remaining assets are passed to the donor’s heirs. Charitable trusts can be a great way to defer taxes on highly appreciated assets and reduce the risks associated with concentrated positions while providing an income stream for the donor. There are also ways to replace the value of the donated property for beneficiaries, if necessary.

Everyone Can Give

Even if you don’t have highly appreciated stock or much cash to give, making simple gifts of time, old clothes, or weekly donations to your church, place of worship, or local community charity will still go a long way. We encourage you to enjoy the gift of giving by incorporating philanthropy into your life.

If you could benefit from a conversation with our advisory team, we would be happy to provide a complimentary consultation.

[1] Walsh, C. (April 2008). Money Spent on Others Can Buy Happiness. The Harvard Gazette.

[2] Leimbery, S, & Gibbons, A. (June, 2008). Life Insurance as a Charitable Planning Tool: Part I. Intangible Personal Property.

Important Disclosure: This material is intended for general informational purposes only. Beacon Pointe Advisors does not offer legal or tax advice. Please consult with the appropriate tax or legal professional regarding your circumstances. This information is not intended and should not be relied upon as individualized tax, legal, fiduciary, or investment advice. Only a tax or legal professional may recommend the application of this general information to any particular situation or prepare an instrument chosen to implement any design discussed herein. Nothing herein should be relied upon as personalized investment advice, nor should it be considered an individualized recommendation, offer or solicitation for the purchase or sale of any security or to adopt a specific investment strategy. An investor should consult with their financial professional before making any investment decisions. Beacon Pointe provides links for your convenience to other providers’ websites. Beacon Pointe is not responsible for errors or omissions in the material on third-party websites and does not necessarily approve or endorse the information provided.