Note: If you are the beneficiary of an inherited retirement account from a loved one, the RMD rules applicable to the inherited retirement account may vary from the information below. To learn more about inherited RMDs, review So You’ve Inherited An IRA.

RMD Basics

What Are Required Minimum Distributions (RMDs)?

The IRS requires a minimum amount to be distributed from most retirement plans annually beginning at a certain age. Required Minimum Distributions (RMDs) apply to most employer-sponsored qualified retirement plans like 401(k)s, 403(b)s, 457(b)s, profit-sharing plans, other defined contribution plans, defined benefit plans, etc., as well as traditional IRAs and IRA-based plans such as SEPs, SARSEPs, and SIMPLE IRAs. RMDs are generally not required during the original owner’s lifetime for Roth IRAs or designated Roth accounts in employer retirement plans, such as Roth 401(k) or Roth 403(b) accounts. However, beneficiaries of inherited Roth IRAs and inherited designated Roth employer-plan accounts are subject to post-death required distribution rules, which may vary based on the beneficiary type and the plan’s terms. RMDs are generally taxed as ordinary income; however, an RMD that is a return of qualified basis is tax-free. You may be able to delay taking RMDs from qualified retirement plans if you are still working.

When Are You Required to Take RMDs?

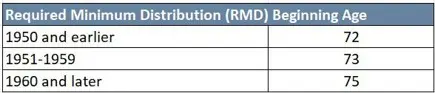

The age account owners must commence taking lifetime RMDs based on their birth year. For individuals born from 1951 through 1959, lifetime RMDs generally begin at age 73. For individuals born in 1960 or later, lifetime RMDs generally begin at age 75. However, if you are still working past the age of 73 and are less than a 5% owner in the company sponsoring the plan, you may delay taking your RMD until the year you retire if the plan allows it (for qualified plans only, not IRAs).

The first RMD must be taken for the year you turn 73 but can be delayed until April 1 of the following year. However, account owners are responsible for taking the correct RMD amount by December 31 of all subsequent years. The penalty for not distributing the minimum required amount is 25% of the amount required to be distributed but not withdrawn.1 This penalty may also be reduced to 10% if the error is corrected timely. However, most individuals who miss an RMD will request a complete penalty waiver.

If you were born before 1952, you should already be taking RMDs. The provisions of the SECURE Act 2.0 increased the required beginning date for RMDs to age 73 starting on January 1, 2023, specifically for individuals born between 1951-1959. Account owners born in 1953 must take their first RMD for 2026, though no later than April 1, 2027. Account owners born in 1960 and beyond, no RMDs are required until age 75. Summarized in the chart below.

Planning Tips

Postponing the first year’s RMD may be a good approach if you estimate that your taxable income or income tax rate in the following year would be substantially lower. However, keep in mind, if you postpone taking your initial RMD, the next year will then require two distributions (one from the previous year plus the current year’s RMD), which may reduce the potential for paying tax at a lower rate. If you don’t need your RMD and are looking for ways to reduce your taxable income, see below on donating your RMD to charity.

How are RMDs Calculated?

RMDs are calculated for each account by dividing the prior year’s December 31 account balance by a life expectancy factor that the IRS publishes. The Uniform Lifetime Table is the most commonly used set of factors. It applies to unmarried account owners, owners with non-spouse beneficiaries, or an owner with a spouse beneficiary not more than 10 years younger. The Joint and Last Survivor Table is used if the account’s sole beneficiary is the owner’s spouse, who is more than 10 years younger. These tables can be found on the IRS website. We recommend working with a CPA to ensure your RMD amount is correct.

Most financial institutions will estimate the amount of the RMD you need to take, and you can work with your Beacon Pointe Client Service Associate to complete the process. To estimate your annual RMD, work with your CPA or try an online calculator. If you recently changed brokerage firms since the end of the prior year, check with your CPA to calculate the RMD for that year.

Note: The IRS updated its life expectancy tables for RMD purposes effective for 2022 and later years. When calculating the RMD for your own IRA, please work with your tax advisor to ensure you utilize the correct tables.

Any excess distribution from one year cannot be applied to future RMDs, and rolling your RMD into another tax-deferred retirement account is not allowed. An RMD must be calculated separately for each IRA account, but you can withdraw the total amount of the RMD from one or more IRAs or 403(b)s. However, separate RMDs are required to be taken from each qualified plan (e.g., 401(k), profit-sharing, and 457(b) accounts).

How Should You Withdraw RMDs?

If your RMD is part of the income that supports your daily living needs, a regular monthly or quarterly distribution allows you to dollar cost average out of the market, timely providing the cash flow needed to meet those needs.

If you do not need the funds to cover your expenses, you could take your RMDs “in-kind” by transferring an equivalent amount of assets directly to a non-retirement investment account rather than selling. For example, if you own a mutual fund now closed to new investors and do not want to liquidate it, an in-kind transfer will preserve your access. Or, you may hold assets in your retirement accounts that you believe to be undervalued. An in-kind transfer can satisfy the RMD while allowing you to benefit from any post-distribution appreciation in a non-retirement account. Note that the distribution of the RMD, even if in-kind, is treated as ordinary income, and any future post-distribution gain in a non- retirement account would benefit from preferential capital gains tax rates.

Should You Consider Directly Transferring Some or All of Your RMD to Charity?

If you are over age 70½, do not need the RMD to cover your expenses, and are charitably inclined, you could donate all or part of that RMD to certain charities to avoid paying income tax on the amount donated. The Qualified Charitable Distribution (QCD) rules allow distributions of up to $111,000 annually (2026) per taxpayer from Traditional or Inherited

IRAs (but not from a SEP or SIMPLE IRA, or an employer retirement plan) to go directly to certain qualified public charities (check with your CPA) and avoid including the distribution as income on your tax return. The limit is adjusted annually for inflation (which started in 2024). QCD donors will not receive an income tax deduction for the charitable donation, but do not have to pay income taxes on that income. If you are no longer itemizing deductions, given the increased standard deduction, you might consider giving through a QCD to reduce your income subject to tax.

Individuals may now make a one-time distribution of up to $55,000 (2026 limit and will adjust with inflation) from an IRA to a charitable gift annuity or charitable remainder trust. The $55,000 is part of the $111,000 overall limit above. These charitable strategies provide an income stream for the individual during their life, and any excess assets at their death benefits charities. Given the lifetime threshold of $55,000, the charitable gift annuity will likely be more beneficial for most taxpayers as the charitable remainder trusts may be more complex and costly for tax and legal expenses.

Withholding Taxes from Your RMD

We suggest working with your CPA to determine the appropriate amount of income tax to withhold on your RMDs (if any). If you are already working with a CPA to estimate quarterly tax payments, you may not need to withhold taxes from your RMDs. Tax withheld from RMDs decreases the amount of estimated tax payments needed and withheld taxes from your RMDs are credited to your estimated tax obligation as if the taxes were paid in equal installments (even if it is not received until late in the year).

1 Effective for 2023, the penalty on missed RMDs is reduced to 25%. Prior to 2023, the penalty on missed RMDs was 50%.

Important Disclosure: Beacon Pointe Advisors does not offer legal or tax advice. Please consult with the appropriate tax or legal professional regarding your circumstances. This information is not intended and should not be relied upon as individualized tax, legal, fiduciary, or investment advice. Only a tax or legal professional may recommend the application of this general information to any particular situation or prepare an instrument chosen to implement any design discussed herein. Nothing herein should be relied upon as personalized investment advice, nor should it be considered an individualized recommendation, offer or solicitation for the purchase or sale of any security or to adopt a specific investment strategy. An investor should consult with their financial professional before making any investment decisions. Beacon Pointe provides links for your convenience to other providers’ websites. Beacon Pointe is not responsible for errors or omissions in the material on third-party websites and does not necessarily approve or endorse the information provided.

Copyright © 2026 Beacon Pointe Advisors, LLC®. No part of this document may be reproduced