The Quick Facts

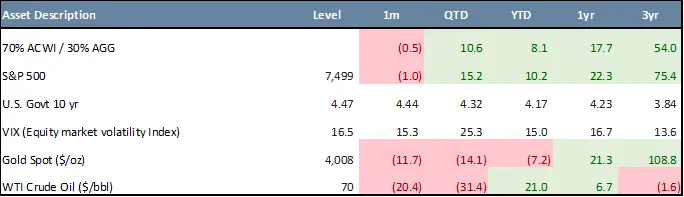

- Balanced portfolios posted a modest setback in June, declining 0.5%, but remained firmly positive at +8.1% year-to-date and +17.7% over one year.

- U.S. equities were mixed following the strong April-May rebound. The S&P 500 fell 1.0% in June but remained up 10.2% year-to-date, while the Nasdaq 100 slipped just 0.1% and held a 20.3% year-to-date gain.

- Leadership rotated beneath the surface, with Industrials (+7.3%), Health Care (+6.6%), and Financials (+4.3%) outperforming, while Communication Services (-7.2%), Energy (-5.0%), and Consumer Discretionary (-2.8%) lagged.

- International equities were mixed but remained constructive overall. MSCI EAFE gained 0.1% in June and 9.9% year-to-date, while MSCI Emerging Markets fell 1.4% for the month but remained up 23.8% year-to-date.

- Fixed income delivered modest gains as Treasury yields edged higher. The U.S. Aggregate Bond Index gained 0.2% in June and 0.6% year-to-date, while High Yield bonds rose 0.3% and remained up 2.0% year-to-date.

- June market sentiment was shaped by the Fed holding rates steady, Iran-related geopolitical risk, the high-profile SpaceX IPO, and sharp monthly declines in gold, oil, and Bitcoin.

* * *

Markets cooled off in June after a strong rebound in April and May, but diversified portfolios remained positive for the year. A balanced portfolio made up of 70% global stocks and 30% U.S. core bonds declined 0.5% for the month, but was still up 8.1% year-to-date and 17.7% over the past year.[1]

Stocks were mixed. The S&P 500 fell 1.0% in June but remained up 10.2% for the year, while the Nasdaq 100 was nearly flat for the month and stayed up 20.3% year-to-date. Market leadership shifted during the month, with areas such as Industrials, Health Care, and Financials doing better, while Communication Services, Energy, and Consumer Discretionary lagged. This shows that different parts of the market can move in different directions, even when the overall market is relatively steady.

International stocks were also mixed but remained positive for the year. Developed international markets were slightly positive in June, while emerging markets declined for the month, but remained one of the strongest areas year-to-date. This highlights the value of global diversification, since returns often vary across regions.

Bonds provided modest support. The U.S. Aggregate Bond Index gained 0.2% in June and was up 0.6% year-to-date, even as Treasury yields moved slightly higher. In simple terms, bond prices and interest rates usually move in opposite directions, so rising yields can limit bond returns. Still, bonds helped provide stability during a month when stocks and commodities were more uneven.

Several headlines influenced investor sentiment in June. The Federal Reserve kept interest rates steady, signaling that it wants more evidence that inflation is under control before shifting policy. Geopolitical tension around Iran affected energy markets, although oil prices fell sharply during the month as earlier concerns eased. The SpaceX IPO drew attention to high-growth companies, while gold, oil, and Bitcoin all posted notable monthly declines.

Overall, June was a pause after a strong second-quarter rally rather than a major change in market direction. The key takeaway for investors is that diversification remains important. Stocks have driven most of this year’s gains, bonds have provided modest stability, and different asset classes continue to respond differently to inflation, interest rates, geopolitics, and investor sentiment.

June Asset Class Performance

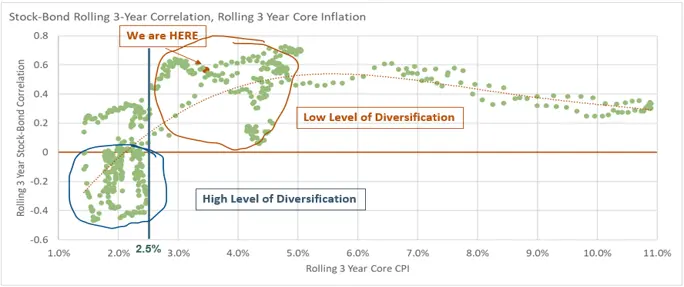

Chart of the Month – Stock-Bond Rolling 3-Year Correlation, Rolling 3 Year Core CPI

This month’s chart focused on the relationship between stocks, bonds, and inflation. Historically, the diversification benefits of a traditional stock-bond portfolio have been strongest during periods of low and stable inflation.

When rolling three-year Core CPI has remained below roughly 2.5%, stocks and bonds have often had a negative correlation. Put simply, when stocks declined, bonds were more likely to help offset some of the weakness. This was a key reason traditional balanced portfolios worked so well for much of the period following the Global Financial Crisis. However, when inflation rises above that approximate 2.5% threshold, the relationship between stocks and bonds can change. Higher inflation can become a major driver of both asset classes. In those environments, rising interest rates and inflationary pressure may weigh on stocks and bonds at the same time, reducing the cushioning effect that bonds have historically provided.

The current environment remains more consistent with this higher-inflation regime. Core inflation is still above the levels historically associated with the strongest stock-bond diversification. That does not mean bonds are no longer useful. It does mean investors should have realistic expectations about how much protection traditional bonds may provide if inflation remains elevated or interest rates stay volatile.

This backdrop highlights the potential value of incorporating alternative investments into a well-diversified portfolio, where appropriate for the investor. Strategies such as private credit, private equity, real assets, infrastructure, hedge funds, and other non-traditional investments may offer return drivers that differ from public stocks and bonds. Alternatives are not a substitute for a thoughtful core portfolio, and they come with their own risks, including reduced liquidity, complexity, and different fee structures. However, for qualified investors with appropriate time horizons and risk tolerance, they can help broaden sources of return and improve overall portfolio resilience. [2]

This is especially relevant when stock-bond correlations are elevated. In that kind of environment, relying only on traditional stocks and bonds may leave portfolios more exposed to the same macroeconomic risks, including inflation, interest rates, and economic growth expectations.

Quote of the Month

“The future is uncertain; therefore, the best strategy is to own assets that respond differently to different economic environments.” — Ray Dalio

Curated by Julien Frazzo, Deputy Chief Investment Officer, and Michael G. Dow, CAIA, CFA®, Chief Investment Officer.

[1] The 70/30 balanced portfolio is a hypothetical index blend and does not represent an actual Beacon Pointe portfolio. Indexes are unmanaged, cannot be invested in directly, and do not reflect fees, expenses, or taxes.

[2] Alternative investments, including funds that invest in alternative investments, are risky and may not be suitable for all investors. Alternative investments often employ leveraging and other speculative practices that increase an investor’s risk of loss to include complete loss of investment, often charge high fees, and can be highly illiquid and volatile.

Related Links

Beacon ‘Pointe of View’ – A Market Update June 2026

Macro & Markets: May 2026 – An Update from Beacon Pointe CIO

Important Disclosure: The information contained in this article is for general informational purposes only. Opinions referenced are as of the publication date and may be modified due to changes in the market or economic conditions and may not necessarily come to pass. Forward-looking statements cannot be guaranteed. Past performance is not a guarantee of future results. Beacon Pointe has exercised all reasonable professional care in preparing this information. The information has been obtained from sources we believe to be reliable; however, Beacon Pointe has not independently verified or attested to the accuracy or authenticity of the information. The discussions, outlook, and viewpoints featured are not intended to be investment advice and do not consider specific investment objectives or risk tolerance you may have. All investments involve risks, including the loss of principal. Consult your financial professional for guidance specific to your circumstances. This document has been prepared with the assistance of ChatGPT Enterprise, an AI-powered tool designed to enhance productivity and provide support in drafting, editing, and organizing content. ChatGPT Enterprise leverages advanced AI models to generate text based on user input. Although ChatGPT Enterprise generates original content based on user input, there is a risk that the generated text may inadvertently resemble existing works that may not be properly cited. AI‑assisted content is reviewed by Beacon Pointe personnel for accuracy, completeness, and compliance.