* * *

The Quick Facts

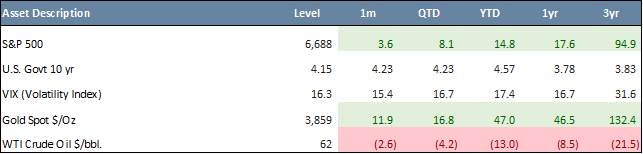

- U.S. markets rose for a fifth straight month in September (S&P 500 +3.6%, Nasdaq +5.5%), driven by tech and AI.

- YTD gains remain strong (S&P +14.8%, Nasdaq +18.1%), though Emerging Markets (“EM”) (+27.5%) and Europe, Australasia, and the Far East (“EAFE”) (+25.8%) continue to lead on U.S. dollar weakness.

- The Federal Reserve (“Fed”) cut interest rates 25 basis points, signaling potential additional cuts later this year.

- Political pressure on the Fed raises concerns about central bank independence.

- Labor market data showed a slowdown while inflation remained above target with Consumer Price (“CPI”) +2.9% YoY, core +3.1%.

- Treasury yields fell, with the 10-Year ending September at 4.15%. Bonds rallied broadly, supported by rate-cut expectations and safe-haven demand.

- Gold surged to record highs (+47% YTD), while oil declined 13% year-to-date. The U.S. dollar was flat in September, down 9.9% YTD, and market volatility remained muted, with the VIX range-bound and the MOVE index at multi-year lows.

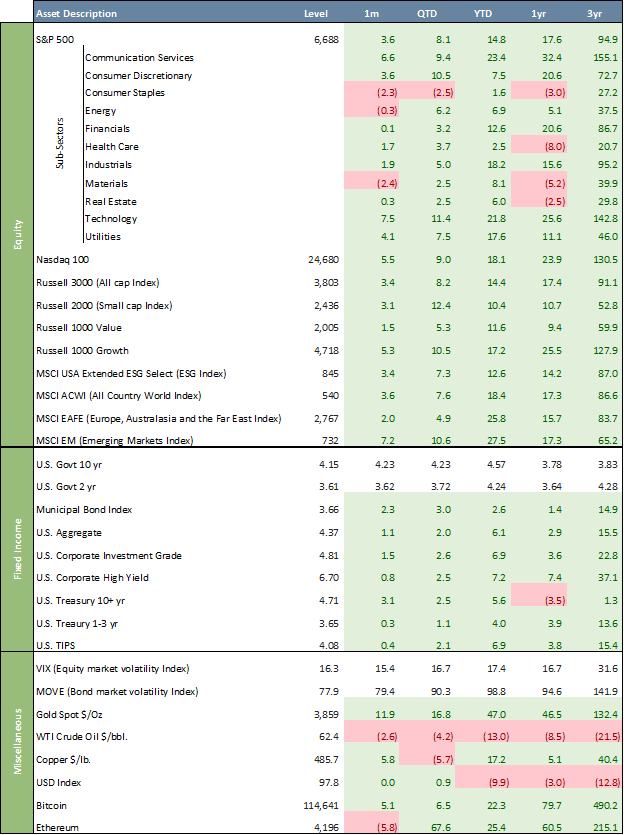

U.S. equities delivered a strong September, defying seasonal patterns, with the S&P 500 rising 3.6% and the Nasdaq up 5.5%. This capped off a solid Q3, where tech and AI-related names drove much of the upside. Investors continue to bet on multiple Fed cuts and durable earnings momentum. YTD, the S&P is up 14.8% and the Nasdaq 18.1%, reflecting a strong rebound from early-year jitters. The S&P 500 posted eight new closing highs for the month and 28 YTD. EM, as measured by the MSCI EM Index, and Europe, Australasia, and EAFE, as measured by the MSCI EAFE Index, remain ahead of U.S. equities with YTD returns of 27.5% and 25.8%, respectively, partly helped by a weakening U.S. dollar.

Global Industry Classification Standard (“GICS”) sectors’ performances were generally positive in September. Most sectors posted gains, led by Information Technology (+7.5%) and Communication Services (+6.6%). Year-to-date, all GICS sectors are in the green with two sectors clearly outperforming, Communication Services up +23.4% and Information Technology up +21.8%, while Consumer Staples is lagging, up just 1.6%.

Septemeber Asset Class Performance

Large Cap Value stocks underperformed Large Cap Growth, with the Russell 1000 Value Index up 1.5% in September (+11.6% YTD), compared to a 5.3% gain for the Russell 1000 Growth Index (+17.2% YTD). Over the past three years, Value has trailed Growth by 68.1%. The ESG segment, as measured by the MSCI USA ESG Select Index, rose 3.4% in September (+12.6% YTD), trailing the S&P 500 by 2.2% YTD. Over three years, the ESG index appreciated 87.0%, underperforming the S&P 500 by 7.9%.

Much of the global market narrative of September continued to center around the Fed. On September 17, the Fed cut interest rates by 25 basis points to 4.00–4.25% amid slowing job growth and moderating economic activity, while continuing its balance sheet reduction. The move, described as a risk-management step, reflected concern about rising unemployment even as inflation remained above target. The new “dot plot” showed expectations for further rate cuts by year’s end, with inflation forecast to ease gradually toward the 2% goal. Political tensions also flared when President Trump attempted, so far unsuccessfully, to remove Fed Governor Lisa Cook, underscoring challenges to the Fed’s independence as it navigated trade-offs between inflation control and labor market support. And on October 1, the U.S. Supreme Court refused to allow President Trump to immediately oust Lisa Cook while she sues to keep her job, dealing a setback to his efforts to exert more control over the central bank.

U.S. macro data painted a mixed picture in September. The labor market showed signs of weakening as private-sector employment fell by 32,000 jobs, as reported by ADP, the sharpest decline in over two years, though jobless claims dropped to 218,000. This suggests that layoffs remain contained, while forecasts point to unemployment drifting towards 4.5%. At the same time, inflation remained sticky, with the August CPI (released in September) rising 2.9% year-over-year and 0.4% month-over-month, while core inflation climbed 3.1% annually, reinforcing concerns that price pressures remain above the Fed’s target. Looking ahead, forecasts suggest CPI will stay near 3%, highlighting the Fed’s challenge of balancing slowing job growth with stubborn inflation, all while markets closely watch its response and commitment to independence. Discussions about the Fed’s “third mandate” related to pursuing moderate long-term interest rates have gained traction as a potential tool for managing the cost of debt – and as a source of tension between the Fed and the administration – the Fed has focused on the dual mandate rather than the more ambiguous “third.”

The fixed income rally sparked by Fed Chair Powell’s Jackson Hole remarks carried through September. The 10-year U.S. Treasury yield ended the month at 4.15%, down from 4.23% in August and well below its October 2023 peak of 4.99%. The 2-year yield closed at 3.61% versus 3.72% at the end of June. Notably, the yield curve dis-inverted in September 2024, with the 10-year now 54 basis points above the 2-year. In Q3, bonds gained on expectations of Fed rate cuts, declining real yields, and safe-haven demand amid macro and fiscal uncertainty. The rally was broad-based, with the Bloomberg U.S. Aggregate Bond Index (AGG) up 2.0%, municipal bonds up 3.0%, investment-grade corporates up 2.6%, and high-yield bonds up 2.5%.

In September, gold surged 11.9% to a record $3,859/oz (+47.0% YTD), reinforcing its role as a hedge against fiat currencies. The rally was driven by weakening U.S. real yields, a softer dollar, and safe-haven demand amid geopolitical and macro uncertainty. Oil (WTI crude) fell another 2.6% to $62.4/bbl, bringing its YTD decline to 13.0%. In digital assets, Bitcoin gained 5.1% in September (+22.3% YTD), while Ethereum slipped 5.8% but remains up 25.4% YTD.

The U.S. Dollar Index (DXY) was flat in September, leaving its YTD decline at 9.9%, pressured by rising market expectations for additional Fed rate cuts and concerns over political interference potentially undermining central bank independence. A weaker DXY enhances U.S. dollar returns on non-U.S. equities, making international stocks more appealing to U.S. investors.

September was calm from a volatility standpoint: the VIX, the so-called “fear gauge,” traded in a narrow 14–19 range, well below its 30-year average of ~20. Meanwhile, the ICE BofA MOVE Index, which tracks U.S. Treasury market volatility, fell further to 73.5, its lowest level since 2021, after spiking to 140 in early April. Extended periods of low VIX often signal investor complacency, suggesting markets may be underestimating potential risks and could be vulnerable to sudden spikes in volatility.

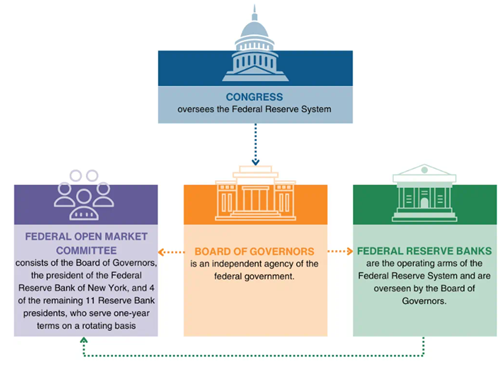

Chart of the Month – Fed Org Chart

The Fed is the most influential central bank because it controls U.S. monetary policy, shaping interest rates, inflation, and growth. Its decisions affect borrowing costs for consumers and businesses, influencing spending, investment, and jobs. Since the U.S. dollar is the world’s reserve currency, Fed policies ripple through global markets, guiding investor behavior and capital flows worldwide.

The Fed’s leadership has two main groups: the Board of Governors and the presidents of 12 regional Reserve Banks. The seven governors, nominated by the President and confirmed by the Senate, serve staggered 14-year terms to limit political pressure. The President also appoints a Chair and Vice Chair from this group for renewable four-year terms. These governors play a central role in shaping monetary policy.

Regional Reserve Bank presidents are selected by their local boards with approval from Washington. Five serve at a time on the Federal Open Market Committee (FOMC), which sets U.S. monetary policy. The New York Fed president has a permanent seat, while four others rotate. This structure balances national and regional perspectives in decision-making.

Independence is critical because it shields policy from short-term political influence. Politicians may favor quick fixes, like rate cuts before elections, even if they fuel inflation later. Long terms and insulated appointments ensure the Fed focuses on stability and sustainable growth. Independence preserves public trust, anchors inflation expectations, and supports a resilient financial system.

Quote of the Month

“Logic, history strongly suggest that a less indepedent central bank is less likely to achieve its objectives, particularly its price-stability objective.” – Donald Kohn (former Fed Vice Chair)

Major Asset Class Dashboard

Curated by Julien Frazzo, Deputy Chief Investment Officer and Michael G. Dow, CAIA, CFA®, Chief Investment Officer

RELATED LINKS

Beacon ‘Pointe of View’ – A Market Update September 2025

Beacon ‘Pointe of View’ – A Market Update August 2025

Important Disclosure:

The information contained in this article is for general informational purposes only. Opinions referenced are as of the publication date and may be modified due to changes in the market or economic conditions and may not necessarily come to pass. Forward-looking statements cannot be guaranteed. Past performance is not a guarantee of future results. Beacon Pointe has exercised all reasonable professional care in preparing this information. The information has been obtained from sources we believe to be reliable; however, Beacon Pointe has not independently verified or attested to the accuracy or authenticity of the information. The discussions, outlook, and viewpoints featured are not intended to be investment advice and do not consider specific investment objectives or risk tolerance you may have. All investments involve risks, including the loss of principal. Consult your financial professional for guidance specific to your circumstances. This document has been prepared with the assistance of Microsoft Copilot, an AI-powered tool designed to enhance productivity and provide support in drafting, editing, and organizing content. Microsoft Copilot leverages advanced AI models to generate text based on user input. Although Copilot generates original content based on user input, there is a risk that the generated text may inadvertently resemble existing works that may not be properly cited.