* * *

The Quick Facts

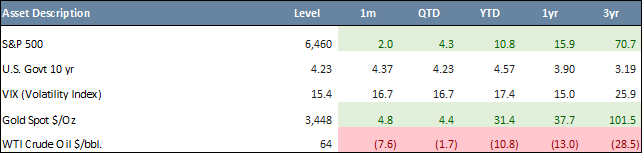

- U.S. equities continued their rally, with the S&P 500 up 2.0% in August (10.8% YTD), driven by optimism over potential Federal Reserve (“Fed”) rate cuts and strong mega-cap tech performance.

- Small-cap stocks outperformed, with the Russell 2000 gaining 7.0%, while international markets led overall gains—MSCI EAFE rose 23.4% and MSCI EM climbed 19.0% YTD.

- Jackson Hole highlighted Fed policy and independence concerns, as Chair Powell signaled possible rate cuts later in the year amid weak labor data. The Fed’s inflation-fighting credibility suffers with political interference.

- Gold and U.S. dollar index (DXY) movements reflected market caution, with gold surging 4.8% to $3,448/oz as investors sought a safe haven amid Fed independence concerns, while the DXY fell 2.2% on expectations of a September rate cut.

U.S. equities posted their fourth consecutive month of gains, with the S&P 500 up 2.0% in August (10.8% YTD). While tariff-related uncertainty and geopolitical tensions continued to weigh on the market, optimism surrounding potential upcoming Fed rate cuts and mega-cap tech strength helped propel the S&P 500 to a new all-time closing high on August 28.

The rally broadened in August, with mid and small caps outperforming their large-cap peers. The Russell 2000 Small cap Index was up 7.0% in August, outperforming the large cap benchmark by 5.0%. Year-to-date through August 31, the S&P 500 gained 10.8%, significantly underperforming international markets. The MSCI EAFE Index surged by 23.4%, driven by strong performance in the Eurozone and other developed markets. The MSCI EM Index rose by 19.0%, supported by robust earnings growth and easing inflation in key emerging economies.

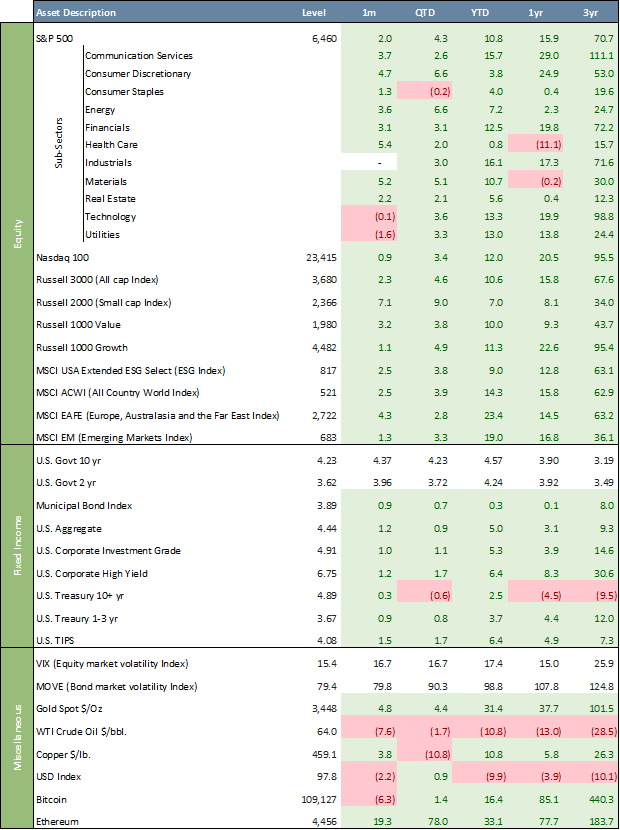

Global Industry Classification Standard (“GICS”) sectors’ performances were generally positive in August. Most sectors posted gains, led by Materials (+5.2%) and Health Care (+5.4%). Utilities (-1.6%) and Technology (-0.1%) were the two decliners. Year-to-date, all GICS sectors are in the green with Industrials (+16.1%) leading and Health Care (+0.8%) lagging.

August Asset Class Performance

Large Cap Value stocks underperformed Large Cap Growth, with the Russell 1000 Value Index up 3.2% in August (+9.3% over 12 months), compared to a 1.1% gain for the Russell 1000 Growth Index (+22.6% over 12 months). Over the past three years, Value has trailed Growth by 51.7%. The ESG segment, as measured by the MSCI USA ESG Select Index, rose 2.5% in August (+9.0% YTD), trailing the S&P 500 by 1.8% YTD. Over three years, the ESG index appreciated 63.2%, underperforming the S&P 500 by 7.6%.

Much of the global market narrative of August centered around the Fed. Investors closely watched Chair Jerome Powell’s remarks at the Jackson Hole Economic Symposium, which struck a cautious balance between acknowledging a weakening labor market and reaffirming the Fed’s inflation-fighting credibility. What overshadowed the usual policy discussions, however, was political drama—namely, President Trump’s attempt to dismiss Fed Governor Lisa Cook. This move fueled speculation that the White House was encroaching on the central bank’s independence, raising questions about whether monetary policy decisions could be swayed by political considerations rather than economic fundamentals.

Markets interpreted the symposium outcome as dovish, thus supportive for risk assets. Powell signaled that rate cuts were possible later in the year if the economy continued to soften, even as he pushed back against overt political pressure. The perception that the Fed’s independence was under attack generated some anxiety to the otherwise bullish market tone. Gold’s outperformance during August reflected a hedging strategy—not just against economic weakness, but against uncertainty at the core of the world’s most influential central bank.

On the inflation front, the July 2025 CPI report, released on August 12, showed headline inflation rising 2.7% year-over-year and core CPI up 3.1%, signaling sticky price pressures. The July 2025 PCE index, published on August 29, recorded 2.6% headline inflation and 2.9% core PCE, keeping the Fed’s preferred gauge above its 2% target. The latest inflation reports show that tariffs are having a slight impact on inflation, though not enough to keep the Fed from cutting interest rates.

Fixed income surged following Fed Chair Powell’s comments at the Jackson Hole symposium, signaling the likelihood of rate cuts resuming in September. The 10-year U.S. Treasury yield closed August at 4.23%, down from 4.37% a month earlier, and down from its October 2023 peak of 4.99%. The 2-year yield ended at 3.62%, down from 3.96% at the end of July. The yield curve dis-inverted in September 2024, with the 10-year now steepening to 61 basis points above the 2-year. Fixed income surged in August with the U.S. Aggregate Bond Index up 1.2% (+5.0% YTD), while the Municipal Bond Index gained 0.9% with the YTD performance now back in positive territory (+0.3%). The U.S. Corporate Investment Grade Index was up 1.0% for the month, bringing the YTD return to 5.3%.

Gold had another strong month in August, up 4.8% ($3,448/oz) with YTD gains of 31.4%. Growing concerns over political interference in the Fed’s independence, heightened fears of inflation and instability in traditional assets, all spurred investors to shift toward the safety of gold. Oil (WTI Crude) dropped 7.6% to $64.0/bbl., and is now down 10.8% YTD. Bitcoin was down 6.3% in July (+16.4% YTD), while Ethereum was up 19.3% (+33.1% YTD). Ethereum’s rally is supported by growing institutional investment, new ETF approvals, and market narratives favoring its fundamental utility in DeFi, NFTs, and smart contracts.

The U.S. Dollar index (“DXY”) was down 2.2% in August, weighed down by growing market expectations for a Fed interest rate cut in September and concerns over political interference undermining central bank independence, bringing the YTD decline to 9.9%. A lower DXY boosts U.S. dollar returns on non-U.S. equities, making international stocks more attractive to U.S. investors.

Other than for a tariff-related spike on August 1, the VIX Index, often called the “fear gauge,” traded in a narrow 14 to 19 range the entire month of August as equity market volatility remains below its 30-year average of ~20. Meanwhile, the ICE BofA MOVE Index (MOVE), which measures U.S. Treasury market volatility, eased further in August, closing at 79.3, after a spike to 140 in early April.

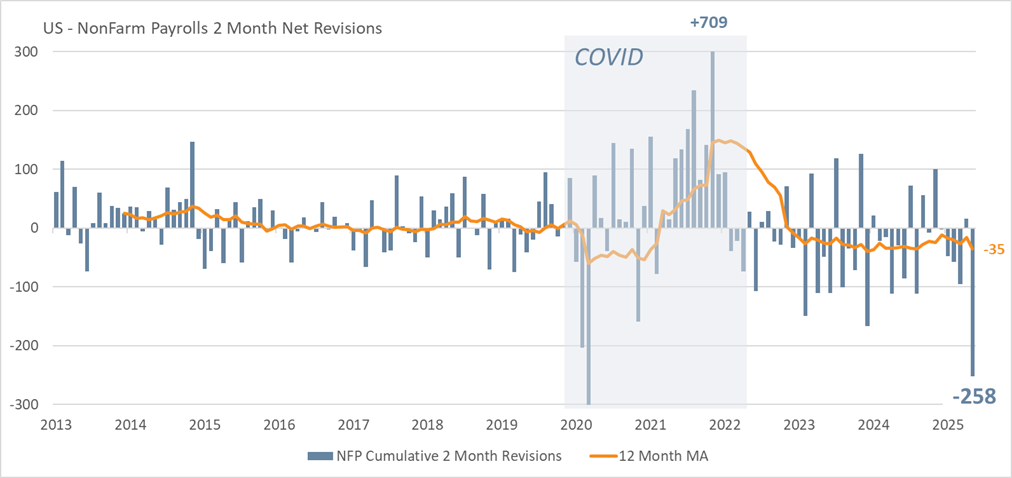

Chart of the Month – Nonfarm Payrolls

Nonfarm payrolls (“NPF”) measure the number of paid employees in the U.S. economy, excluding farm workers, private household employees, and some government/military workers. They come from the Current Employment Statistics (“CES”) survey, which is run by the Bureau of Labor Statistics (“BLS”). The CES surveys about 119,000 businesses and government agencies each month, covering over 600,000 worksites.

NFP is the core figure in the monthly jobs report, released on the first Friday of each month. NFP is revised because the initial payroll estimate is based on incomplete survey responses, and more accurate data arrives in the following weeks. Revisions also account for updated business records, seasonal adjustments, and annual benchmarking against unemployment insurance records.

The initial estimate (the “first print”) is based on about 65–70% of the survey responses received by the deadline. As more businesses submit their data later, the BLS updates the figures in the next two months’ reports. Once a year, the BLS aligns its survey-based estimates with the more comprehensive Quarterly Census of Employment and Wages (“QCEW”), which uses unemployment insurance records from nearly every employer. This “benchmarking” process can lead to very large adjustments—hundreds of thousands of jobs added or subtracted.

July 2025’s steep downward revision to NFP was an outlier, with over 250,000 jobs erased—far larger than the typical adjustment of around 10,000. But it was not unique, as past turning points like the 2008 financial crisis, the 2011 strike-related swings, and recent benchmark revisions have also produced very large shifts. The unexpected firing of the BLS head shortly after the weak July jobs report appears unjustified, given that large downward revisions have occurred historically at key turning points and are not unusual.

U.S. NFP Revisions: 2013 to Present

Quote of the Month

“Employment numbers, such as nonfarm payrolls, are crucial indicators of the economy’s health, but they must be interpreted in context, not in isolation.” – Ben Bernanke (former Fed Chair)

Major Asset Class Dashboard

Curated by Julien Frazzo, Deputy Chief Investment Officer and Michael G. Dow, CAIA, CFA®, Chief Investment Officer

RELATED LINKS

Beacon ‘Pointe of View’ – A Market Update August 2025

Macro & Markets: August 2025 – An Update from Chief Investment Officer, Michael G. Dow

Important Disclosure:

The information contained in this article is for general informational purposes only. Opinions referenced are as of the publication date and may be modified due to changes in the market or economic conditions and may not necessarily come to pass. Forward-looking statements cannot be guaranteed. Past performance is not a guarantee of future results. Beacon Pointe has exercised all reasonable professional care in preparing this information. The information has been obtained from sources we believe to be reliable; however, Beacon Pointe has not independently verified or attested to the accuracy or authenticity of the information. The discussions, outlook, and viewpoints featured are not intended to be investment advice and do not consider specific investment objectives or risk tolerance you may have. All investments involve risks, including the loss of principal. Consult your financial professional for guidance specific to your circumstances. This document has been prepared with the assistance of Microsoft Copilot, an AI-powered tool designed to enhance productivity and provide support in drafting, editing, and organizing content. Microsoft Copilot leverages advanced AI models to generate text based on user input. Although Copilot generates original content based on user input, there is a risk that the generated text may inadvertently resemble existing works that may not be properly cited.