The Internal Revenue Service (IRS) has released the updated annual limits and thresholds for retirement plans for the 2026 tax year, reflecting cost‑of‑living adjustments. These limits apply to contribution amounts and benefit caps across various qualified retirement plans.

Key Takeaways:

- The IRS has published the annual limits on contributions and benefits for retirement plans for the 2026 tax year.

- Annual contribution limits are adjusted based on cost‑of‑living increases.

- The maximum elective deferral for 401(k), 403(b), and most 457(b) plans is increased to $24,500 for 2026.

- Catch‑up contribution limits for employees aged 50 and over have a higher threshold under the updated guidelines.

- Individual Retirement Account (IRA) contribution limits are adjusted for 2026.

- Annual additions and benefit limits for defined contribution and defined benefit plans reflect updated IRS tables.

- Retirement plan sponsors and payroll systems require updates to reflect these new annual limits for compliance.

* * *

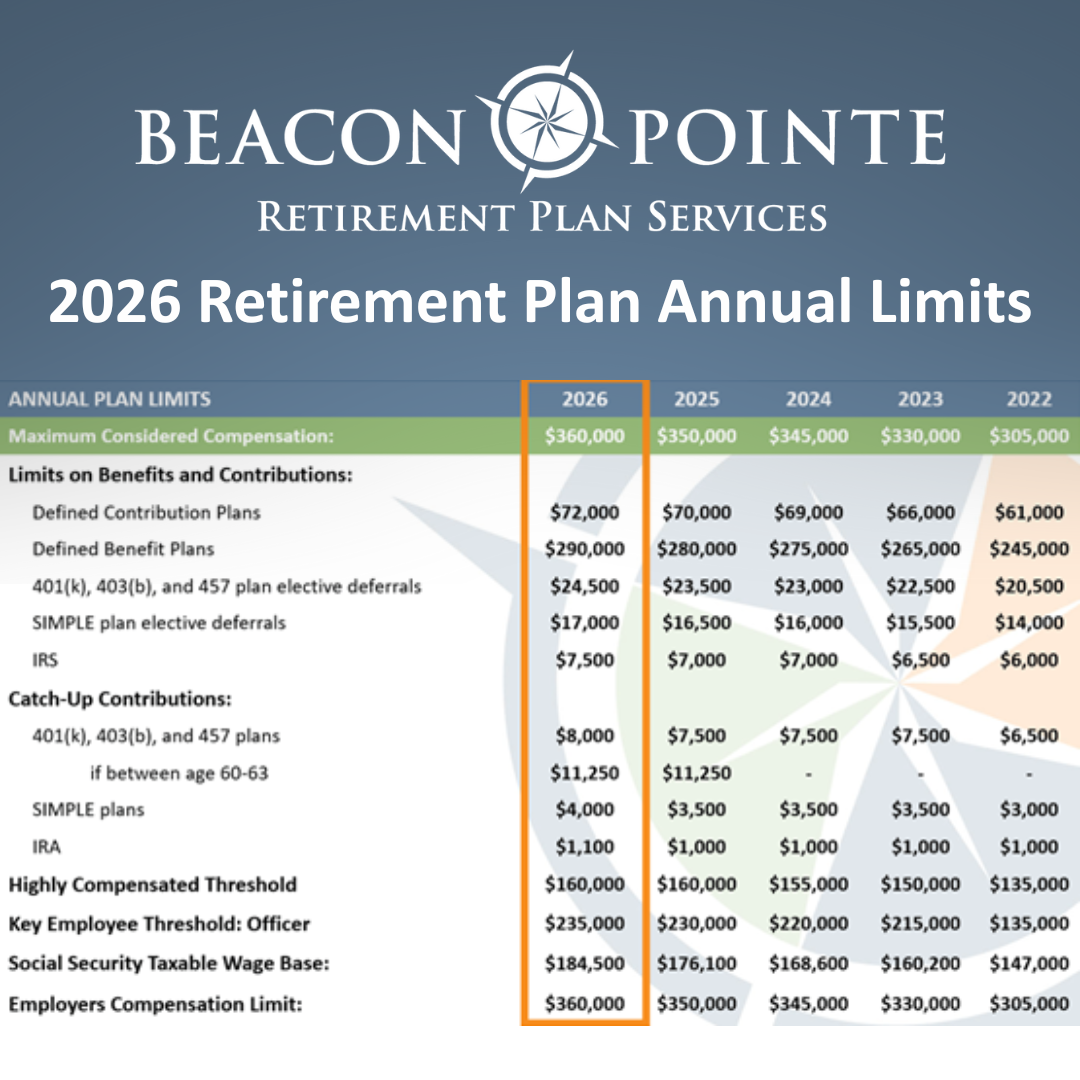

Awareness of the current annual limits may support individuals and employers in tracking allowable contribution amounts and required administrative updates for retirement plan reporting and participation. Below is a chart outlining the limits on benefits and contributions for a variety of retirement plan options, along with catch-up contributions for 2026.

Annual Plan Limits |

2026 |

2025 |

2024 |

2023 |

2022 |

|---|---|---|---|---|---|

| Maximum Considered Compensation: | $360,000 | $350,000 | $345,000 | $330,000 | $305,000 |

Limits on Benefits and Contributions: |

|||||

| Defined Contribution Plans | $72,000 | $70,000 | $69,000 | $66,000 | $61,000 |

| Defined Benefit Plans | $290,000 | $280,000 | $275,000 | $265,000 | $245,000 |

| 401(k), 403(b), and 457 plan elective deferrals | $24,500 | $23,500 | $23,000 | $22,500 | $20,500 |

| SIMPLE plan elective deferrals | $17,000 | $16,500 | $16,000 | $15,500 | $14,000 |

| IRS | $7,500 | $7,000 | $7,000 | $6,500 | $6,000 |

Catch Up Contributions: |

|||||

| 401(k), 403(b), and 457 plans | $8,000 | $7,500 | $7,500 | $7,500 | $6,500 |

| 401(k), 403(b), and 457 plans (if between age 60-63) | $11,250 | $11,250 | – | – | – |

| SIMPLE plans | $4,000 | $3,500 | $3,500 | $3,500 | $3,000 |

| IRA | $1,100 | $1,000 | $1,000 | $1,000 | $1,000 |

Highly Compensated Threshold |

$160,000 | $160,000 | $155,000 | $150,000 | $135,000 |

Key Employee Threshold: Officer |

$235,000 | $230,000 | $220,000 | $215,000 | $135,00 |

Social Security Taxable Wage Base: |

$184,500 | $176,100 | $168,600 | $160,200 | $147,000 |

Employers Compensation Limit: |

$360,000 | $350,000 | $345,000 | $330,000 | $305,000 |

Frequently Asked Questions About 401k Plans

What is a 401K plan?

A retirement savings plan employers offer to their employees.

How do I put money into a 401k account?

You contribute money directly from your paycheck with pre-tax and/or after-tax dollars.

Why should I participate in my employer’s 401k retirement plan?

By contributing to the plan, you are saving money for your retirement while receiving tax benefits now or in the future depending on your contribution type.

How is my account invested?

Depending on your company’s plan, there are several investments to choose from which consist of stocks, bonds, and cash-type instruments.

What is a match?

Your employer may offer a matching contribution based on the amount you decide to contribute to your own 401(k) plan. The amount varies by employer.

What is a vesting schedule?

A vesting schedule states how many years an employee must work to own a percentage of the contribution the employer provides.

What happens to my retirement account if I leave my employer?

You have a few options if you decide to leave your employer. These options consist of leaving your money with your past employer, rolling your 401(k) into your new employer, establishing an Individual Retirement Account (‘IRA’) where you may roll your 401(k) into, or cashing out. Please note, each option may have tax ramifications that you will want to confirm with your financial advisor or tax accountant.

Will I be penalized if I take my money out of my retirement account?

If you are under 59 ½ and terminated from your employer, the IRS imposes a 10% early withdrawal penalty if you cash out.

How can I access my money while still employed?

Some employer plans may allow for loans. Check with the plan administrator or read the plans Summary Plan Description.

Source: www.irs.gov.

Important Disclosure: The information set forth herein is for illustrative and informational purposes only and is solely for use only in connection with the purposes for which it is presented. This information is not an investment recommendation, and not meant as tax or legal advice. Please consult with the appropriate tax or legal professional regarding your particular circumstances before making any investment decisions. Beacon Pointe does not endorse and is not responsible for the content, product, or services of other third-party sources. CIRCULAR 230 NOTICE: To ensure compliance with requirements imposed by the IRS, this notice is to inform you that any tax advice included in this communication, including any attachments, is not intended or written to be used, and cannot be used, for the purpose of avoiding any federal tax penalty or promoting, marketing, or recommending to another party any transaction or matter.