The Quick Facts

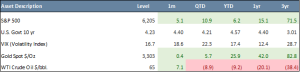

- U.S. equities continued their recovery, with the S&P 500 up 5.1%.

- Growth stocks outpaced Value by 3.0%, with the Russell 1000 Growth Index gaining 6.4% in June, while U.S. stocks outperformed Developed international markets.

- Concerns about stagflation from tariffs have put the Federal Reserve (Fed) in a position where they are waiting for more data before resuming rate cuts.

- Relatively soft inflation prints lessened tariff inflation fears, which lowered yields across the curve.

- Markets generally shrugged off the Israel-Iran “12-day war” with the S&P 500 finishing at all-time-highs.

- First quarter GDP was revised lower due to the lowest growth in consumer spending since the onset of the pandemic.

U.S. equities continued their strong rebound in June, despite heightened geopolitical tensions. The S&P 500 climbed 5.1% for the month (+6.2% year-to-date). Growth stocks continued their strong comeback, outperforming Value by 3.0% in June, but similar year-to-date returns.

Although June saw a “12-day war” between Israel and Iran, oil (WTI Crude) prices only rose 7.1% to $65.1/bbl. and the CBOE Volatility Index (VIX) remained muted, finishing at 16.7, below its 30-year average of 20.1.

Emerging Markets (EM) outperformed U.S. Large Caps equities and Europe, Australasia, and the Far East (EAFE) equities in June. Year-to-date returns stand at +15.3%, +6.2% and +19.9%, respectively.

First quarter GDP was revised down from -0.2% to -0.5% due to U.S. consumer spending growing at the weakest pace since the onset of the pandemic. Spending on services contributed 0.3% to GDP in the first three months of the year, down sharply from the previously reported 0.8% boost. All seven major categories of services spending were revised lower in the final official figures.

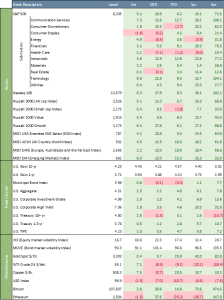

June Asset Class Performance

The Global Industry Classification Standard (GICS) sectors mostly posted gains in June. Ten out of eleven sectors rose, led by Technology (+9.8%), Communication Services (+7.3%), and Energy (+4.9%). Consumer Staples was the only sector to decline (-1.6%).

Large Cap Value stocks underperformed Large Cap Growth, with the Russell 1000 Value Index up 3.4% in June (+13.7% over 12 months), compared to a 6.4% gain for the Russell 1000 Growth Index (+17.2% over 12 months). Over the past three years, Value has trailed Growth by 55.5%.

The Russell 2000 Index, a key measure of smaller companies, also had a strong June, returning 5.4% (-1.8% YTD). The ESG segment, as measured by the MSCI USA ESG Select Index, rose 4.1% in June (+5.0% YTD), trailing the S&P 500 by 1.2% YTD. Over three years, the ESG index appreciated 64.8%, underperforming the S&P 500 by 6.7%.

Developed non-U.S. equities underperformed U.S. equities in June, while Emerging Markets equities outperformed. The EAFE Index rose 2.2%, while the EM Index gained 6.0%. Over the past three years, both EAFE and EM have lagged U.S. Large Caps by 12.7% and 39.5%, respectively.

At the June 18, 2025, Fed meeting, the central bank held interest rates steady at a target range of 4.25% to 4.5%, unchanged since December 2024. Concerns about stagflation from tariffs have put the Fed in a position where they are waiting for more data before resuming rate cuts.

The U.S. Treasury market experienced lower volatility in June compared to May, with a 20% decline in standard deviation, driven by inflation prints that came in below expectations which helped ease tariff-driven inflation concerns. Compounding interest expense remains one of the primary challenges to maintaining a sustainable federal budget; therefore, lower inflation—which increases the probability of Fed rate cuts—helps alleviate fears that the government will be forced to refinance debt at higher rates.

The 10-year U.S. Treasury yield closed June at 4.23%, down from 4.40% a month earlier, and down from its October 2023 peak of 4.99%. The 2-year yield ended at 3.72%, down from 3.90% in May. The yield curve dis-inverted in September 2024, with the 10-year now 51 basis points above the 2-year. The U.S. Aggregate Bond Index was up 1.5% in June (+4.0% YTD), while the Municipal Bond Index rose 0.6% (-0.3% YTD). The U.S. Corporate Investment Grade Index was up 1.9% for the month and up 4.2% YTD.

June saw some progress on tariffs. The European Union (EU) is open to a trade deal with the U.S. that includes a 10% universal tariff on many of its exports, provided that lower rates apply to key sectors such as pharmaceuticals, alcohol, semiconductors, and commercial aircraft. Additionally, the EU is seeking quotas and exemptions to mitigate the impact of the U.S.’s 25% tariff on automobiles and car parts and the 50% tariff on steel and aluminum.

On June 13, Israel launched preemptive strikes on Iranian nuclear facilities and other key targets, triggering a 12-day war that concluded with a U.S.-brokered ceasefire on June 23, effectively ending hostilities by June 25. Despite intense geopolitical tensions, global financial markets remained remarkably stable: safe-haven assets such as U.S. Treasuries and the dollar saw minimal inflows, equity indices dipped briefly but rebounded quickly, and oil spiked by approximately 11% before retreating.

Gold was flat in June ($3,303/Oz) with YTD gains of 25.9%, driven by safe-haven demand. Oil (WTI Crude) gained 7.1% to $65.1/bbl., yet still down 9.2% YTD. Bitcoin extended its May gains, ending May at ~107,600, up 2.6% for the month as investors continued to seek alternatives to traditional assets amid macroeconomic uncertainty.

The U.S. Dollar Index (DXY) fell 2.5% in June, bringing its YTD decline to 10.7%, amid concerns over fiscal sustainability and the U.S. dollar’s global reserve status.

The VIX Index, often called the “fear gauge,” declined from 18.6 at the beginning of the month to 16.7 as equity market volatility eased amid improving sentiment, below its 30 year average of 20.1. Meanwhile, The ICE BofA MOVE Index (MOVE), which measures U.S. Treasury market volatility, eased further in June, closing at 90.3, after a spike to 140 in early April.

Chart of the Month – The Importance of Strategy: Emotions of the Market

Markets naturally rise and fall and reacting emotionally to these short-term swings can lead to poor timing. Many investors buy when prices are high out of excitement, then sell when prices drop out of fear, which is the opposite of a sound investment approach. Sticking to a long-term plan means staying calm during downturns and resisting the urge to chase hot trends during market booms. Emotions like fear, greed, and anxiety can influence decision-making, causing investors to abandon strategies, overreact to headlines, or misjudge risks altogether.

Chasing the latest shiny objects in investing—like trending technologies or hyped sectors—often means buying into assets after much of the upside has already been priced in. This can expose investors to overvaluation risk and sharp corrections if expectations aren’t met. It can also lead to a reactive, short-term mindset, diverting attention from fundamentals and long-term value. Instead of consistent gains, this strategy often results in buying high and selling low. If a new technology is truly transformative, it should eventually be reflected in the composition of broad-based indexes like the S&P 500 or MSCI All Country World Index (ACWI). These indexes are designed to adapt and evolve—rising companies gain weight, while declining ones fall away. In other words, patient investors who stick with a diversified portfolio could still benefit from innovation without the risks of speculative timing or stock picking.

Historically, those who remain disciplined — who stay invested through the highs and lows — tend to perform better than those who frequently jump in and out of the market. Over time, we believe consistency and patience prove far more valuable than attempts to time the market or react to every fluctuation.

Importance of a Strategy: Emotions of the Market

Quote of the Month

“Emotions are the enemy of rational decision-making.” – Todd Combs

Major Asset Class Dashboard

Curated by Julien Frazzo, Deputy Chief Investment Officer and Michael G. Dow, CAIA, CFA®, Chief Investment Officer

RELATED LINKS

Beacon ‘Pointe of View’ – A Market Update June 2025

Beacon ‘Pointe of View’ – A Market Update May 2025

Important Disclosure: The information contained in this article is for general informational purposes only. Opinions referenced are as of the publication date and may be modified due to changes in the market or economic conditions and may not necessarily come to pass. Forward-looking statements cannot be guaranteed. Past performance is not a guarantee of future results. Beacon Pointe has exercised all reasonable professional care in preparing this information. The information has been obtained from sources we believe to be reliable; however, Beacon Pointe has not independently verified or attested to the accuracy or authenticity of the information. The discussions, outlook, and viewpoints featured are not intended to be investment advice and do not consider specific investment objectives or risk tolerance you may have. All investments involve risks, including the loss of principal. Consult your financial professional for guidance specific to your circumstances. This document has been prepared with the assistance of Microsoft Copilot, an AI-powered tool designed to enhance productivity and provide support in drafting, editing, and organizing content. Microsoft Copilot leverages advanced AI models to generate text based on user input. Although Copilot generates original content based on user input, there is a risk that the generated text may inadvertently resemble existing works that may not be properly cited.