The Quick Facts

- U.S. equities posted double-digit gains for a third straight year in 2025, with the S&P 500 up 17.9% after a rapid rebound from an April sell-off driven by tariff concerns.

- Mega-cap strength and AI optimism led performance, while easing financial conditions helped broaden gains to Mid and Small caps later in the year.

- Non-U.S. equities outperformed meaningfully, with Emerging Markets (“EM”) and Europe, Australasia, and Far East (“EAFE”) rising over 30%, aided by a weaker U.S. dollar.

- All sectors finished higher, though leadership remained concentrated in Technology and Communication Services.

- Fixed income delivered its strongest year since 2020 as the Federal Reserve (“Fed”) cut rates three times and Treasury yields declined.

- Economic growth remained solid but moderated, with softer labor data and easing inflation guiding a shift toward less restrictive Fed policy.

- Gold surged 64.6% to $4,319/Oz while oil ($57.4/bbl.) and Bitcoin ($87,648) fell 19.9% and 6.5%, respectively in 2025.

* * *

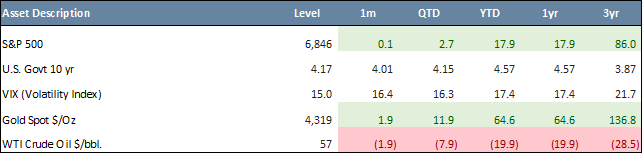

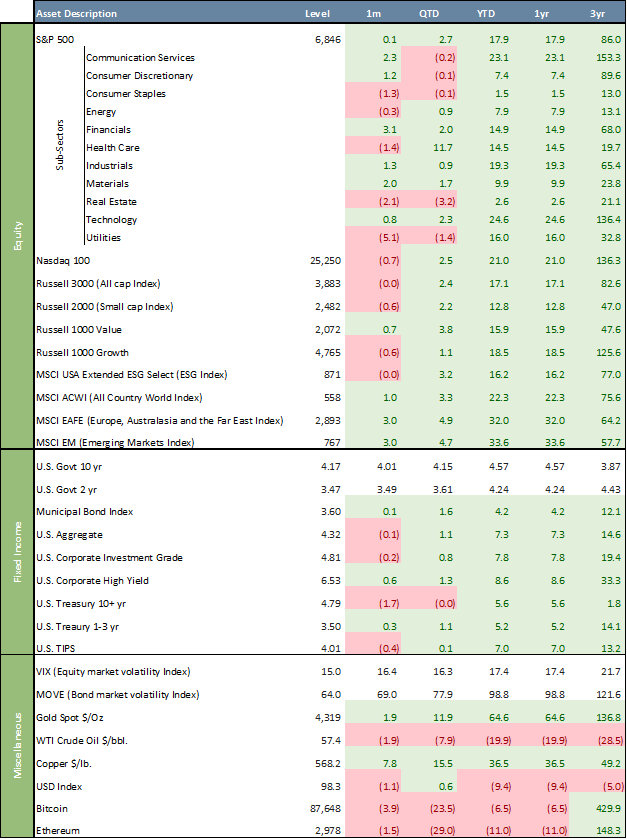

U.S. equities capped 2025 with double-digit gains for the third year in a row, witnessing one of the most rapid recoveries on record after approaching bear market territory in early April. The S&P 500 gained 17.9% in 2025 (0.1% in December and 2.7% in Q4) and posted 39 record closing highs, amid geopolitical, tariff, and inflation-related tensions coupled with a government shutdown and labor market concerns.

The market’s comeback was powered by mega-cap strength and steadfast AI-related optimism. Enthusiasm for Fed rate cuts also propelled the rally to broaden towards Mid and Small caps, with the Russell 2000 Index up 12.8% in 2025. The Magnificent 7 outperformed the broader Large cap benchmark with a 24.9% return in 2025. All eleven Global Industry Classification Standard (“GICS”) sectors ended 2025 higher, led by Information Technology and Communication Services, up 24.6% and 23.1%, respectively, while Consumer Staples and Real Estate lagged, up 1.5% and 2.6%, respectively. Non-U.S. equities significantly outperformed, with EM and EAFE up 33.6% and 32.0%, respectively, driven by strong rallies in Europe and Asia, and a weaker U.S. dollar that boosted foreign returns in USD terms.

December Asset Class Performance

Large Cap Value stocks outperformed Large Cap Growth stocks, with the Russell 1000 Value Index up 0.7% in December (+15.9% in 2025), compared to a 0.6% loss for the Russell 1000 Growth Index (+18.5% in 2025). Over the past three years, Value has trailed Growth by 77.9%. The ESG segment, as measured by the MSCI USA ESG Select Index, was flat in December (+16.2% in 2025), trailing the S&P 500 by 1.7% in 2025. Over three years, the ESG index appreciated 77.0%, underperforming the S&P 500 by 9.0%.

Yields moved unevenly in December, but U.S. Treasuries posted their strongest year of returns since 2020. The 10-year U.S. Treasury yield ended 2025 at 4.17%, from 4.57% a year ago and well below its October 2023 peak of 4.99%. The 2-year yield closed at 3.47%, versus 4.24% a year ago. The yield curve dis-inverted in September 2024, with the 10-year now 69 basis points above the 2-year. U.S. fixed income delivered solid positive returns in 2025 as spreads compressed, and the Fed cut rates. The rally was broad-based, with the Bloomberg U.S. Aggregate Bond Index (“AGG”) up 7.3% in 2025, municipal bonds up 4.2%, investment-grade corporates up 7.8%, and high-yield bonds up 8.6%.

Despite some large quarterly swings, the U.S. economy looks set to turn in a solid year of growth for 2025, a trend economists expect to continue in 2026. The economy expanded 4.3% in the third quarter, the fastest pace in two years, thanks to resilient consumer spending and business investment. Economic reports returned with the November employment report showing a net gain of 64,000 jobs. Unemployment rose to 4.6% in November, from 4.1% in December 2024. The Consumer Price Index (“CPI”) rose at a 2.7% annualized rate in November, a delayed report from the Bureau of Labor Statistics showed.

After holding rates steady early in the year, the Fed delivered three quarter-point cuts, bringing the federal funds target range down to 3.50%–3.75% by year-end, the lowest level in nearly three years. Inflation measures continued to drift closer to target while job growth slowed, quit rates fell, and unemployment edged higher, reinforcing the view that policy no longer needed to remain overtly restrictive. Financial conditions eased modestly as a result, with borrowing costs declining and risk assets stabilizing, though the Fed remained careful to avoid signaling a rapid or aggressive easing path. At the same time, policymakers emphasized that the shift reflected risk management rather than victory over inflation. Growth indicators pointed to moderation rather than contraction: consumer spending cooled, business investment softened, and surveys showed weakening confidence among households and firms. Within the Federal Open Market Committee (“FOMC”), divisions became more visible, with some officials arguing for a faster pace of cuts to prevent unnecessary labor market damage, while others warned that inflation could prove sticky and that premature easing risked reigniting price pressures. Chair Powell consistently framed policy as “data-dependent,” underscoring that future moves would hinge on continued progress on inflation and labor rebalancing, leaving markets to price a slower, more conditional path of easing in 2026.

In December, gold advanced another 1.9% to a record $4,319/Oz (+64.6% in 2025), confirming its role as a hedge against fiat currencies. The rally in gold is driven by weakening U.S. real yields, a softer dollar, and safe-haven demand amid geopolitical and macro uncertainty. Oil (WTI crude) fell another 1.9% to $57.4/bbl., bringing its YTD decline to 19.9%. In digital assets, Bitcoin lost 3.9% in December, bringing the 2025 decline to 6.5%, while Ethereum dropped 1.5% for a 2025 decline of 11.0%. The U.S. Dollar Index (“DXY”) was down 1.1% in December, increasing its 2025 decline to 9.4%. A weaker DXY enhances U.S. dollar returns on non-U.S. equities, making international stocks more appealing to U.S. investors.

The VIX, the so-called “fear gauge,” closed 2025 at 15.0, below its 30-year average of ~20. In April, the VIX soared sharply, briefly climbing above 50 amid tariff-driven market panic and an equity sell-off tied to U.S.–China trade tensions, marking the largest volatility spike since COVID. Meanwhile, the ICE BofA MOVE Index, which tracks U.S. Treasury market volatility, ended 2025 at 64.0, close to its lowest level (58.5) since 2021 after spiking to 140 in early April.

Market attention now turns to 2026, where expectations center on modest additional rate cuts, possibly one or two, dependent on inflation and employment data. The transition to a new Fed chair in mid-2026 adds a layer of uncertainty to the monetary outlook.

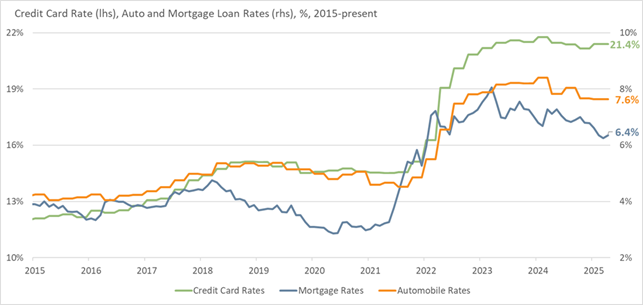

Chart of the Month – Credit Card, Auto, and Mortgage Loan Rates, %

Mortgage, auto, and credit card interest rates have risen sharply since the pandemic, fundamentally changing the cost of borrowing for U.S. consumers. In the years leading up to 2020, interest rates across these categories were near historic lows, supported by accommodative monetary policy and subdued inflation. That environment has reversed. As the Fed moved aggressively to combat post-pandemic inflation, benchmark rates increased at the fastest pace in decades, pushing borrowing costs materially higher across nearly every consumer credit channel.

Mortgage rates illustrate the shift most clearly. Thirty-year fixed mortgage rates that averaged around 3% before the pandemic more than doubled at their peak, dramatically increasing monthly payments for new buyers and freezing housing affordability. Even as rates have come off their highs, they remain far above pre-2020 levels. The result has been reduced transaction volume, constrained housing supply, and sustained pressure on household budgets for those who must finance at current rates. Auto loan rates have followed a similar trajectory. New and used car financing costs rose in tandem with higher policy rates and tighter credit standards, compounding the impact of elevated vehicle prices. Monthly payments have climbed meaningfully, stretching loan terms longer and forcing many consumers to either downgrade vehicle choices or delay purchases altogether. For households that are reliant on auto credit, higher rates translate directly into less disposable income and greater sensitivity to economic shocks. Credit card rates, which are typically variable and closely tied to short-term interest rates, have increased the most consistently and remain at record highs. Unlike mortgages or auto loans, credit card balances often finance everyday expenses, meaning higher rates act as a persistent drag on household cash flow. As interest charges absorb a larger share of monthly payments, consumers face growing difficulty paying down balances, increasing the risk of revolving debt and financial stress.

Collectively, higher mortgage, auto, and credit card rates have raised the cost of money across the economy, squeezing consumers and reinforcing the slowdown in discretionary spending.

Quote of the Month

“If I borrowed money at 18% or 20%, I’d be broke.” – Warren Buffett

Major Asset Class Dashboard

Curated by Julien Frazzo, Deputy Chief Investment Officer, and Michael G. Dow, CAIA, CFA®, Chief Investment Officer.

RELATED LINKS

Beacon ‘Pointe of View’ – A Market Update December 2025

Important Disclosure: The information contained in this article is for general informational purposes only. Opinions referenced are as of the publication date and may be modified due to changes in the market or economic conditions and may not necessarily come to pass. Forward-looking statements cannot be guaranteed. Past performance is not a guarantee of future results. Beacon Pointe has exercised all reasonable professional care in preparing this information. The information has been obtained from sources we believe to be reliable; however, Beacon Pointe has not independently verified or attested to the accuracy or authenticity of the information. The discussions, outlook, and viewpoints featured are not intended to be investment advice and do not consider specific investment objectives or risk tolerance you may have. All investments involve risks, including the loss of principal. Consult your financial professional for guidance specific to your circumstances. This document has been prepared with the assistance of Microsoft Copilot, an AI-powered tool designed to enhance productivity and provide support in drafting, editing, and organizing content. Microsoft Copilot leverages advanced AI models to generate text based on user input. Although Copilot generates original content based on user input, there is a risk that the generated text may inadvertently resemble existing works that may not be properly cited.