Authored by :

Michael G. Dow, CAIA, CFA, CPA, Chief Investment Officer

Julien R. Frazzo, Director of Risk Management and Securities Research

* * *

The Quick Facts

- The Federal Reserve (Fed) hikes rates 425 bps in total in 2022 vs. expectations of just 75 bps a year ago

- Worst year for U.S. equities since 2008, leaving the S&P 500 with an annual decline of 18.1%

- Value outperforms Growth by 21.6% in 2022, the second widest margin on record

- The worst loss ever for the Bloomberg Aggregate Bond Market Index (AGG) at -13.0%

- Alternative investments offer respite for suffering investors in 2022

- Inflation and employment measures stubbornly high

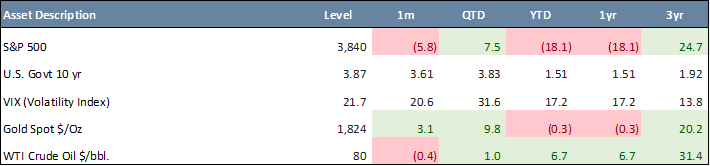

2022 was a tumultuous year, characterized by rate hikes, sticky inflation, and geopolitical tensions, with significant losses across asset classes. A turnaround that began in October was short-lived, leaving the S&P 500 with an annual decline of 18.1%, the worst since 2008. There was no “Santa rally” either, with December down 5.8%.

The bond market also saw one of its worst years in history. It was easily the worst year for the U.S. Aggregate Bond Index, which dates to 1976. In the 45+ years of calendar year returns, there were only four down years before 2022 (-2.9% in 1994, -2.0% in 2013, -1.5% in 2021, and -0.8% in 1999). The total return of -13.0% in 2022 was by far the worst loss ever. Add it all up, and a 60/40 portfolio of U.S. stocks and bonds was down 16.1% in 2022, the third worst year ever for a diversified portfolio.

Inflation measures reached 40-year highs resulting from stimulative fiscal and monetary policies, shifting consumer spending towards goods from services, robust employment, supply chain disruptions, the Ukraine war, and China’s Zero-COVID policies. While the Fed might have been slow off the mark in fighting inflation in 2021, they were much more aggressive in 2022, taking the benchmark Fed Funds rate from 0.0% – 0.25% to 4.25% – 4.5%. At the start of 2022, markets were pricing in just three 25 bps rate hikes.

December Asset Class Performance

According to FactSet, 4Q 2022 earnings for the S&P 500 are expected to decline 2.8%, while calendar year earnings are expected to grow 5.1%, down from estimates of 9.1% on June 30. Although earnings grew 5.1% last year, the increase in inflation and concurrent rise in long-term interest rates led to a significant de-rating of stocks. A key question for markets in 2023 is whether we get an earnings recession or not. Given the prospect of a recession in 2023, the 4.4% consensus growth in earnings by the market appears to be optimistic. There are some hopeful signs that inflation may have peaked, but long-term interest rates may remain sticky should elements of inflation become structural.

U.S. equity benchmarks had their worst annual performance since 2008, which included declines over the first three quarters of 2022. The Nasdaq Composite (-32.5%) was the laggard due in large part to the strong weighting of its mega-cap, growth-style members, which were disproportionately impacted by the historic rise in rates. On a total return basis, only two of eleven GICS (Global Industry Classification Standard) sectors finished in the green after all eleven posted robust double-digit gains in 2021. Energy (+64.2%) led all sectors. The defensive Utilities, Staples, and Healthcare sectors finished at about breakeven. The growth-heavy Communication Services, Consumer Discretionary, and Technology were the laggards, posting negative returns of -37.6%, -36.3%, and -27.7%, respectively.

Aided by the fastest rate hike cycle since 1981, Value outperformed Growth by more than 20% in 2022, which marks its second-best outperformance on record going back to the inception of the Russell indices in 1979. The Russell 1000 Value was down 4.0% in December, outperforming the Russell 1000 Growth by 3.6% in December and a record 21.6% for calendar 2022. The outperformance of Value over Growth continues to be a major investment theme in an environment where long-dated cashflows are discounted at higher rates. The ESG segment of the market, as measured by the MSCI USA ESG Select Index, was down 5.8% in December, in line with the S&P 500. Over the last three years, the ESG index is up 28.8% and approximately 4.0% ahead of the S&P 500 on a total return basis.

The Fed’s hawkish pivot from a transitory inflation outlook in 2021 had the most profound impact on rates and spreads. The shorter 2-year U.S. Treasury yield, most sensitive to the Fed’s monetary policy, rose more than 400 bps to a high of 4.72% in early November before ending the year at 4.43%. The longer-dated 10-year U.S. Treasury yield rose as much as 273 bps to a high of 4.24% in October before closing the year at 3.87%. It is unlikely that the Fed will pivot to easier monetary policy until they are convinced that the Fed Funds rate is positive in real terms and that the labor market is cooling.

Commodities were unusually volatile in 2022 due in large part to Russia’s invasion of Ukraine back in late February. Oil prices, as measured by the WTI Crude Oil $/bbl., peaked in March at $123.70 (+64.5%) before finishing at $80.26 (+6.7%). Precious metals surged late in the year, leaving spot gold with a modest decline of -0.3% (+9.8% in 4Q 2022). Cryptocurrencies, the so-called future of investing, have fared even worse with Bitcoin and Ethereum down 64.3% and 67.5% respectively in 2022, undermined by the end of free money and a wave of bankruptcies, most strikingly, the FTX collapse. The U.S. Dollar Index (DXY) was up as much as 18.9% at its peak in September, which, if held into year-end, would have marked its biggest annual gain on record. However, with the central banks of Europe and Japan becoming increasingly hawkish, the DXY gave up more than half its peak gains before finishing with a gain of 8.2% in 2022.

The CBOE Volatility Index (or VIX), also known as the fear gauge, remained elevated at the end of 2022 at 21.7. While equity investors look to the VIX index as a measure of volatility, bond investors focus on the ICE BofA MOVE (MOVE) Index, which measures bond market volatility. The MOVE Index more than doubled last year and remains elevated at 122, but ~25% off the 161 high recorded in October 2022. When markets are volatile, it is easy to get discouraged and feel tempted to capitulate. Some level of volatility is normal. We caution against making significant changes to your portfolio when things get rocky. Sticking with your investing plan and keeping your money in the market is generally the best way to come out on top in the long run.

Chart of the Month – Long-Term Capital Market Assumptions

The Beacon Pointe investment team relies on Long Term Capital Market Assumptions (LTCMAs) to construct optimal portfolios for our clients and maximize risk-adjusted returns. We believe valuations and higher yields mean that asset markets today may offer the best long-term returns in more than a decade. After a year of turmoil, the core principles of investing still hold firm. Once again, 60/40 can form the bedrock of portfolios, while alternatives can offer alpha, inflation protection, and diversification. The end of free money, greater two-way risk in inflation and policy, and increased return dispersion across assets also give active managers more to swing for.

Long-term return projections have shifted meaningfully higher. The forecasted annual return for a USD 60/40 stock-bond portfolio over the next 10–15 years jumped from 4.1% last year to 7.0% in 2023. While many investors are rightly focused on elevated inflation and other near-term headwinds, inflation is expected to cool over the next couple of years, removing the headwind of restrictive Fed policy.

As policy rates normalized in 2022, bonds again look attractive – they offer a plausible source of income as well as diversification. Higher riskless rates also translate to improved credit return forecasts. Projected equity returns rose sharply – the developed market equity forecast increased nearly 360 bps to 8.80%, and emerging market equities jumped 320 bps to 10.1%. Corporate profit margins will likely recede from today’s levels but not revert completely to their long-term average.

Stock and bond valuations present an attractive entry point. Alternatives still offer benefits (diversification, risk reduction) not easily found elsewhere. With the U.S. dollar more overvalued than at any time since the 1980s, the foreign exchange translation could be a significant component of forecasted returns.

Quote of the Month

“How many millionaires do you know who have become wealthy by investing in savings accounts? I rest my case.” — Robert G. Allen

Major Asset Class Dashboard

RELATED LINKS

Beacon ‘Pointe of View’ – A Market Update December 2022

Macro & Markets: An Update from the CIO February 2023

Important Disclosure: This report is for informational purposes only. Opinions expressed herein are subject to change without notice. Beacon Pointe has exercised all reasonable professional care in preparing this information. The information has been obtained from sources we believe to be reliable; however, Beacon Pointe has not independently verified, or attested to, the accuracy or authenticity of the information. Nothing contained herein should be construed or relied upon as investment, legal or tax advice. All investments involve risks, including the loss of principal. Investors should consult with their financial professional before making any investment decisions. Past performance is not a guarantee of future results.