The Quick Facts

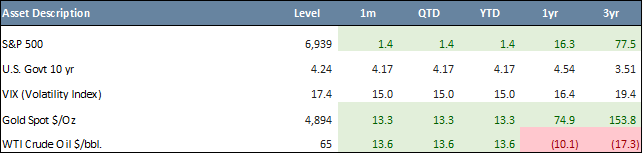

- U.S. equities were volatile in January, with the S&P 500 dropping 2.1% on January 20 but closing positive 1.4% for the month.

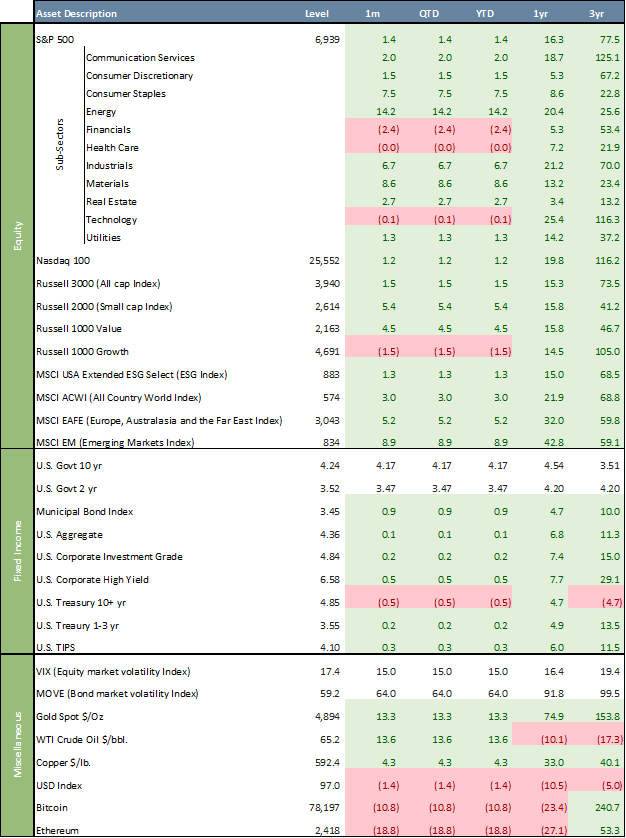

- Sector rotation favored Energy (+14.2%) and Materials (+8.6%), while Financials lagged (-2.4%).

- Small caps (+5.4%) and Value (+4.5%) outperformed Growth (-1.5%) amid mixed tech earnings and inflation concerns.

- Non-U.S. equities outperformed with Europe, Australasia, and Far East (‘EAFE”) up 5.2% and Emerging Markets (“EM”) up 8.9%, aided by a weaker U.S. dollar (-1.4%).

- Fixed income posted modest gains, with the Bloomberg U.S. Aggregate (“AGG”) up 0.1% and 10-year Treasuries at 4.24%.

- Federal Reserve (“Fed”) uncertainty drove markets. Department of Justice (“DOJ”) subpoenas for Powell and Warsh’s nomination heightened concerns over central bank independence.

- Commodities were volatile. Gold surged +13.3% to record highs before retreating, oil rose 13.6%, while crypto fell sharply (BTC -10.8%, ETH -18.8%).

* * *

January proved to be a busy and turbulent start to the year, marked by a string of headline‑making geopolitical and policy developments, including dramatic events in Venezuela, Greenland and Iran, grand jury subpoenas involving the Fed, and President Trump’s nomination of Kevin Warsh as the next Fed Chair, alongside significant market stress such as the Japanese Government Bond sell‑off and a roughly $350 billion wipeout in Microsoft’s market capitalization. On January 20, a sell‑off in Japanese government bonds combined with tariff‑related tensions sparked the S&P 500’s worst single‑day drop since October 2025 (‑2.1%) and pushed the VIX above 20, underscoring heightened risk aversion. Despite this early volatility and subdued reactions to Big Tech earnings, fresh inflation jitters and uncertainty around Fed leadership weighing on sentiment, the market rebounded, with the S&P 500 reaching new all‑time highs and closing the month up 1.4%. EAFE and EM significantly outperformed U.S. equities with 5.2% and 8.9% gains, respectively, helped by a weaker U.S. dollar (-1.4%) that boosted foreign returns in USD terms.

January Asset Class Performance

Most of the eleven Global Industry Classification Standard (“GICS”) large-cap sectors finished higher, led by a rotation toward Energy (+14.2%) and Materials (+8.6%), with Financials lagging (-2.4%). The Russell 2000 (small caps) Index outperformed with a 5.4% gain, albeit with late-month volatility. Large Cap Value stocks outperformed Large Cap Growth stocks, with the Russell 1000 Value Index up 4.5% in January (+15.9% in 2025), compared to a 1.5% loss for the Russell 1000 Growth Index (+18.5% in 2025). Over the past three years, Value has trailed Growth by 58.3%. The ESG segment, as measured by the MSCI USA ESG Select Index, was up 1.3% in January (+16.2% in 2025), trailing the S&P 500 by 0.1%. Over three years, the ESG index appreciated 68.5%, underperforming the S&P 500 by 9.0%.

Yields moved unevenly in January. The 10-year U.S. Treasury yield ended January at 4.24%, from 4.17% at the end of December and well below its October 2023 peak of 4.99%. The 2-year yield closed at 3.52%, versus 3.47% at the end of December. The yield curve dis-inverted in September 2024, with the 10-year now 71 basis points above the 2-year. U.S. fixed income delivered positive returns in January as spreads compressed. The positive performance was broad-based, with the U.S. AGG up 0.1% in January, municipal bonds up 0.9%, investment-grade corporates up 0.2%, and high-yield bonds up 0.5%.

On the macroeconomic front, U.S. business activity remained steady and inflation data stayed moderate, but geopolitical tensions, including U.S. policy conflicts and trade disputes, weighed on sentiment globally. Fed policy and leadership were at the center of intense political and market attention as Fed Chair Jerome Powell revealed that the DOJ had served the Fed with grand jury subpoenas, part of a criminal investigation into his congressional testimony on renovation spending, which Powell vehemently condemned as an unprecedented threat to central bank independence and a politically motivated attempt to force the Fed into deeper rate cuts, heightening concerns about institutional autonomy. Amid these tensions, the Federal Open Market Committee (“FOMC”) chose to hold interest rates steady after a series of cuts in 2025, signaling that policymakers saw no compelling reason for further reductions in January despite political pressure. The political climate was further shaken at the end of the month when President Trump nominated former Fed governor Kevin Warsh to succeed Powell as Chair, a decision that injected both clarity and controversy into the future of U.S. monetary policy given Warsh’s “hawkish” reputation and the hotly debated confirmation prospects in a closely divided Senate. Warsh’s nomination immediately influenced markets, boosting the dollar while triggering sharp selloffs in gold and precious metals, as investors priced in potential shifts in policy direction. Simultaneously, Senator Thom Tillis and other lawmakers vowed to block confirmations of Fed nominees until the DOJ matter involving Powell was resolved, underscoring ongoing partisan clashes over both Fed independence and the direction of interest rate policy.

Gold continued a historic bull run in January (+13.3%), pushing to all-time highs close to $5,500 per ounce as investors rushed into the metal early in the month on safe-haven demand amid global economic and geopolitical uncertainty, expectations of monetary easing, central bank buying and a weaker U.S. dollar, extending the massive rally that began in 2025. However, late in the month that strength was met with intense volatility and a sharp correction as speculative positioning peaked, margin requirement hikes and shifting expectations around Fed policy triggered profit taking and forced liquidations, leading gold to pull back substantially from its highs toward the month’s end. Oil (WTI crude) gained 13.6% to $65.2/bbl., driven by escalating tensions in the Middle East. January 2026 was a weak month for crypto markets. Bitcoin lost 10.8%, while Ethereum dropped 18.8%. The U.S. Dollar Index (“DXY”) was down 1.4% in January, increasing its 12-month decline to 10.5%. A weaker DXY enhances U.S. dollar returns on non-U.S. equities, making international stocks more appealing to U.S. investors.

The VIX, the so-called “fear gauge,” started the month relatively calm around the mid-14s then climbed modestly through the month as markets faced geopolitical and macroeconomic uncertainty, notably spiking above 20 around January 20 amid tariff and policy concerns before drifting lower by month-end, averaging roughly ~16 for January, below its 30-year average of ~20. Meanwhile, the ICE BofA MOVE Index, which tracks U.S. Treasury market volatility, ended January at 59.2, close to its lowest level (56.2) since 2021 after spiking to 140 in early April.

Chart of the Month – Interest Paid on U.S. Treasury Public Debt Outstanding, $ billions

The Interest Paid on U.S. Treasury Public Debt Outstanding is the amount the federal government pays each year in interest on debt held by the public (investors, foreign governments and the Federal Reserve). It reflects the cost of borrowing through Treasury bills, notes and bonds when spending exceeds tax revenue. The figure is reported in billions of dollars as part of the federal budget.

This interest is one of the government’s largest expenses and is growing quickly. When debt levels rise or interest rates go up, the cost of servicing that debt increases automatically. High interest payments matter because they consume tax dollars that could otherwise fund programs like defense, infrastructure or social spending, and they limit future fiscal flexibility.

Interest costs have surged in recent years as both total debt and interest rates have increased. Net interest spending is now the top federal outlay and is projected to keep rising. Interest expense on the national debt now exceeds spending on national defense and is at the highest level as a percentage of tax receipts (18.6%) since the mid-90s. This trend has intensified debates in Washington about deficits, borrowing and long-term debt sustainability.

Economists and budget analysts are highlighting that if current trends persist, annual debt-service costs could reach upward of $1–1.8 trillion over the next decade, potentially crowding out other priorities and fueling debates over fiscal policy and debt sustainability.

Quote of the Month

“The boom, not the slump, is the right time for austerity at the Treasury.” – John Maynard Keynes

Major Asset Class Dashboard

Curated by Julien Frazzo, Deputy Chief Investment Officer, and Michael G. Dow, CAIA, CFA®, Chief Investment Officer.

RELATED LINKS

Beacon ‘Pointe of View’ – A Market Update January 2026

Important Disclosure: The information contained in this article is for general informational purposes only. Opinions referenced are as of the publication date and may be modified due to changes in the market or economic conditions and may not necessarily come to pass. Forward-looking statements cannot be guaranteed. Past performance is not a guarantee of future results. Beacon Pointe has exercised all reasonable professional care in preparing this information. The information has been obtained from sources we believe to be reliable; however, Beacon Pointe has not independently verified or attested to the accuracy or authenticity of the information. The discussions, outlook, and viewpoints featured are not intended to be investment advice and do not consider specific investment objectives or risk tolerance you may have. All investments involve risks, including the loss of principal. Consult your financial professional for guidance specific to your circumstances. This document has been prepared with the assistance of Microsoft Copilot, an AI-powered tool designed to enhance productivity and provide support in drafting, editing, and organizing content. Microsoft Copilot leverages advanced AI models to generate text based on user input. Although Copilot generates original content based on user input, there is a risk that the generated text may inadvertently resemble existing works that may not be properly cited.