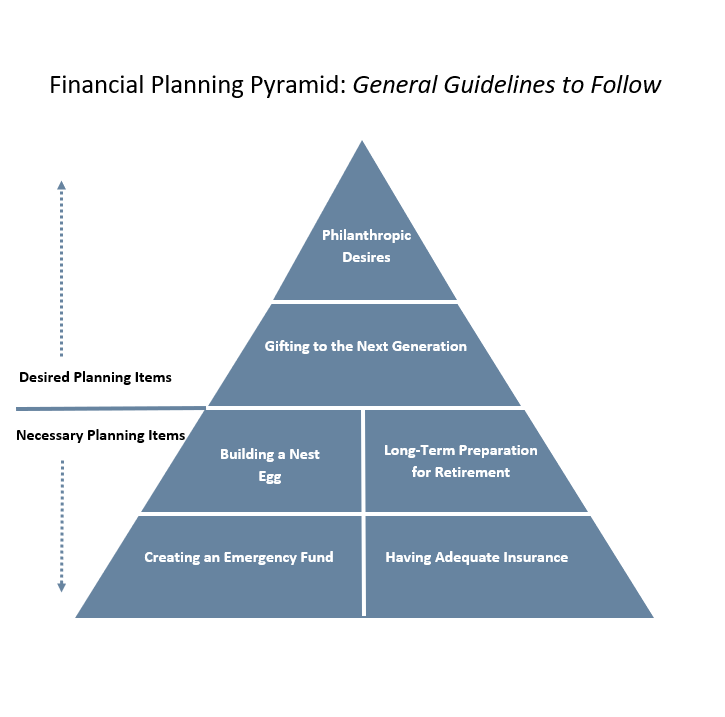

The question of what to address first from a planning perspective, often comes up when starting a financial planning dialogue. The answer depends largely on what you have already addressed. As with most things, it helps to have a good foundation and build from there. While the financial planning pyramid below creates a starting point for a discussion, it is not meant to create hard and fast rules. For example, one doesn’t have to achieve financial independence to make annual donations to charity. On the other hand, if you are considering giving a large portion of your estate away, a more in depth planning discussion is warranted to make sure the topics at the bottom of the pyramid have been adequately addressed.

Start with a Strong Foundation

The foundation of the financial planning pyramid is meant to help you and your family in the case of an emergency or catastrophic event. It is the “cover yourself” section. Nothing is worse than creating a nest egg, and having an external event upend your financial future. Therefore the foundation includes:

• Creating an emergency fund: 6-12 months of expenses in straight cash is recommended. Six months is typically adequate if job and health are strong, and income streams are stable. More is recommended if income ebbs and flows.

• Insurance: This includes things such as having adequate health, disability, life, and umbrella insurance.

Financial Independence and Estate Planning

Once you have covered yourself for emergencies, the next two areas of focus are on building financial independence and estate planning. Both of these are still below the line in the “necessary” part of the pyramid. Whether it is called “building a nest egg,” “preparing for retirement,” or “creating financial independence,” planning and saving for these events provides the ability to make choices later in life. One of these choices is to work or not to work (retirement). Another is to continue to work in the same capacity as you do now vs. pursuing another interest or passion which may not pay as well. No matter what your desired path, the old adage that no one will loan you money to retire is indeed true, which is why proper planning falls into the “necessary” category.

Some may argue that estate planning is not “necessary,” but the fact is that if you don’t deal with it directly, you are allowing the state to make important decisions for you. These decisions include:

• deciding who will take care of your children

• addressing important health care directive needs

• deciding how your estate will be divided

• deciding who will take care of you and your finances if you are incapacitated

While estate taxes aren’t as big a concern as they once were, given the $5.34mm exemption amount per person (as of 2014), in some states probate still is a large potential problem. In California specifically, any estate with assets without a designated beneficiary above $150,000 is subject to probate. The probate fees are charged on the gross estate, and it is a public process.

Optional Planning Items

The two planning pieces which are best looked at once the others are addressed include Philanthropic Desires and Gifting to the Next Generation. Often people and/or parents with large estates are interested in making sizable gifts to one or both of these. This brings up two important planning items:

• Can the gifts be made with enough assets left over to support all other needs?

• If so, what is the best structure of the gift?

The financial planning pyramid points out the importance of addressing the first question first, before getting into the more complex discussion of the various vehicles which can be used. Many estates have varying needs and potential obligations to weigh before making a large gift. Most gifts to charity and to the next generation are irrevocable, so should be considered from all angles before made.

Important Disclosure: This content is for informational purposes only. Opinions expressed herein are subject to change without notice. Beacon Pointe has exercised all reasonable professional care in preparing this information. Some information may have been obtained from third-party sources we believe to be reliable; however, Beacon Pointe has not independently verified, or attested to, the accuracy or authenticity of the information. Nothing contained herein should be construed or relied upon as investment, legal or tax advice. Only private legal counsel may recommend the application of this general information to any particular situation or prepare an instrument chosen to implement the design discussed herein. An investor should consult with their financial professional before making any investment decisions.